The Big Picture on If And When to Refinance Rental Property:

-

- Refinancing is most advantageous when interest rates drop significantly compared to your current mortgage, allowing you to reduce monthly payments and improve cash flow.

- Landlords can leverage cash-out refinancing to access property equity, using the funds for renovations or purchasing additional rental properties. This strategy supports portfolio expansion without depleting savings.

- Refinancing decisions should align with long-term financial objectives, such as switching to fixed-rate loans for stability or shortening loan terms to build equity faster and reduce interest costs over time.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

Mortgage brokers love to tell you they can lower your mortgage payment by refinancing your rental property.

Sometimes, they actually can.

But is it worth refinancing, even then?

Before rushing into a rental property refinance, understand the true costs.

Why Investors Refinance Rental Property

A lower monthly payment means stronger cash flow on your rental property. All investors love passive income — it’s why people become landlords in the first place.

Perhaps the mortgage lender offers to refinance you at a lower interest rate. Or perhaps you want to switch from a 30-year mortgage to a 15-year loan or vice versa.

And, of course, some lenders tempt you with cash out. You start drooling over all the uses you could put that money toward, from new rental property down payments to renovations to personal uses like home remodeling.

Some investing strategies revolve around refinancing. For example, it’s a crucial step in the BRRRR method of real estate investing. Refinancing creates the possibility of infinite returns on real estate investments.

Not all investors have a choice, either. If you borrow a balloon mortgage, you must pay it off before the term expires. That means either selling, refinancing, or finding creative financing.

Here’s a quick run-down of all common benefits of refinancing.

| Benefit | Description |

|---|---|

| Lower Interest Rates | Reduces monthly payments and total interest over the life of the loan. |

| Switch Loan Types | Allows transitioning from an adjustable-rate to a fixed-rate loan for stability. |

| Access to Equity (Cash-Out) | Extracts built-up equity for renovations or purchasing additional properties. |

| Shorten Loan Term | Refinancing into a shorter term helps build equity faster and reduces interest. |

| Increase Cash Flow | Lower payments improve cash flow, increasing profitability and flexibility. |

| Debt Consolidation | Combines multiple loans into one, simplifying management and potentially lowering costs. |

| Portfolio Growth | Frees up capital for expanding rental portfolios without depleting savings. |

The Downsides to Refinancing

You should not take refinancing lightly. Before signing on any dotted lines, consider these drawbacks to refinancing an investment property.

High Closing Costs

Refinancing is expensive. According to LendingTree, the average mortgage refinance costs $4,345 for homeowners borrowing cheaper mortgages.

Can you think of a few things you’d rather do with that money? I can, and they don’t involve handing it to 25-year-old mortgage bankers to blow on a wild weekend in Vegas.

Your loan officer will quickly assure you they’ll roll all closing costs into the loan. That doesn’t make the costs disappear; it just means you can pay interest on their fees.

So your first question must be, “How many years will it take me to recover the closing costs of the refinance in monthly savings?” The answer probably won’t make you happy.

But that’s just the tip of the iceberg.

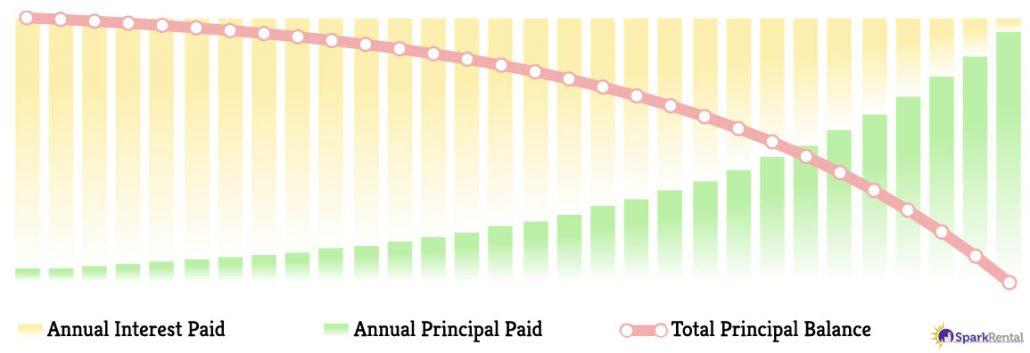

Restarting Your Amortization Schedule

A higher portion of your monthly payment goes toward paying down your principal balance each month in your current loan. The principal paydown schedule is based on what mortgage bankers call “simple interest amortization.”

And there’s nothing simple about it.

The first mortgage payment is always the worst: most of the payment goes to interest for the bank, and a tiny fraction goes toward paying down your principal balance. The next month, slightly less goes to interest, and a little more goes toward principal. This change is gradual initially, then starts picking up speed in the second half of your loan.

Banks never want to see borrowers get to this point in their mortgage payments. They want you to keep refinancing so that they can charge you more up-front fees and keep your monthly payment mostly interest.

It’s in the bank’s best interest (pun intended) to keep refinancing you so that you never get far enough into your loan to really start paying down your balance.

So, the further you get in your loan, the more aggressively they’ll push refinance offers.

Use our free loan amortization calculator to view the full amortization schedule for any loan before signing on the dotted line.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Longer Debt Horizon

I know: 15 or 30 years from now feels like an eternity. But mortgage lenders count on you thinking that way, so that refinancing just feels like moving from one eternity of debt to another.

But if you don’t refinance, you will pay down your mortgage debt over time. Eventually, you’ll pay it off entirely, owning your investment property free and clearly. At that point, your cash flow explodes.

Don’t keep pushing your debt payoff date further into the future. Aim to pay off all your investment property loans sooner rather than later.

When Should Investors Refinance Rental Property?

As outlined above, some investment strategies bake in refinancing from the start. While the BRRRR strategy isn’t for everyone, it’s a perfect example of how refinancing can make sense for investors.

If interest rates plummet and you can drop from a 9% interest rate to a 4% mortgage rate, that also makes sense. Likewise, you may need to pay off a balloon loan due soon.

The earlier you are in your amortization schedule, the less you sacrifice by restarting at Square 1. But the further along you are, the closer you are to real progress in paying down your principal balance with each payment. If your original mortgage was a good one, it rarely makes sense to refinance.

Alternatives to Refinancing Rental Property

“But what if I want to borrow more money?”

I’ll spare you the lecture on borrowing money for non-essential things like vacations or a new bathroom. If you want to borrow money, consider some alternatives with potentially lower costs and stakes.

For flexible financing, consider home equity lines of credit (HELOCs)—or, in this case, rental property equity lines of credit.

You can also open unsecured business lines of credit as a real estate investor. Check out this explainer video from Fund&Grow to learn how to open $100-250K in unsecured credit.

I’ve used credit cards to fund renovations for investment properties. Both personal and business credit cards are an option as well. You can use Plastiq to avoid cash advance fees and limits, you don’t have any closing costs, and you get reward points.

More experienced real estate investors often borrow all the money they need from friends and family. These private money loans may not even have fees.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

How to Refinance a Rental Property

Decided that refinancing your investment makes the most sense for your specific situation? Here’s how you do it:

-

- Assess Goals: Identify the reason for refinancing—lowering interest rates, accessing equity, or changing loan terms.

- Check Credit and Finances: Ensure your credit score and debt-to-income ratio meet lender criteria for the best rates.

- Evaluate Property Value: Obtain an appraisal to confirm the property’s market value and available equity.

- Shop for Lenders: Compare multiple lenders to secure favorable rates and terms.

- Gather Documentation: Collect financial documents like tax returns, bank statements, and proof of rental income.

- Apply for the Loan: Submit your refinance application with the necessary paperwork.

- Complete the Appraisal: The lender may require an independent appraisal to finalize the process.

- Review Loan Terms: Carefully inspect loan agreements, including fees and closing costs, to avoid surprises.

- Close the Loan: Sign the documents, and the new loan will pay off the previous mortgage.

- Manage the New Loan: Start payments under the new terms and adjust your financial strategy accordingly.

Additional Considerations

Before diving in, landlords need to check on a few more things.

Start by exploring both portfolio and conventional lenders. Portfolio lenders come with plenty of advantages, most notably that they don’t limit the number of mortgages that can appear on your credit history. They also don’t appear on your credit report, can close faster than traditional mortgage lenders, and offer far more flexibility.

Portfolio lenders also make borrowing a mortgage for an LLC-owned property much easier.

However, traditional lenders charge slightly lower interest rates in some cases. Compare actual prequalified interest rates at Credible*, or compare portfolio lenders on our rental property mortgages page.

Borrowers with excellent credit scores can borrow an 80-90 loan-to-value ratio (LTV). Weaker borrowers can expect to borrow 60-70% LTV, and they’ll pay higher mortgage rates.

As you establish relationships with specific portfolio lenders, you can often secure discounted interest rates and fees. The better your relationship with a lender, the more likely they offer flexible loan requirements.

You can also try calling local and regional banks to ask if they offer investment property mortgages. It takes more work, but you could find a hidden gem of a lender offering flexible loan terms and affordable loan rates.

Mortgage Rates Now

Here’s a quick overview of today’s mortgage interest rates:

| Owner-Occupied Mortgages for House Hacking | Conventional Mortgages for Investment Properties | Long-Term Portfolio Mortgages | Short-Term Fix & Flip Loans | Private Lenders & Seller Financing | |

|---|---|---|---|---|---|

| Where to Check Rates | Try Credible | Try Credible | Try Kiavi, Visio, or Forman Loans | Try Kiavi, Forman Loans, Civic, or New Silver | Ask people you know! |

| Loan to Value (LTV) | 80-97% | 80-97% owner-occ, 75-80% investors | Up to 80% | Up to 90% + 100% of renovation costs | Negotiable |

| Credit Score | 500+ | 620+ | 600+ | 575+ | No minimum |

| Debt-to-Income Ratio (DTI) | 28% - 36% | 28% - 36% | No income docs required | No income docs required | No income docs required |

| Cash Reserve Requirements | 6-12 mos.' payments | 6-12 mos.' payments | 0-6 mos.' payments | 0-6 mos.' payments | None |

| Interest Rates | 15-Year: 5.375% - 6.25%; 30-Year: 6.124% - 6.99% | 15-Year: 5.25% - 6.49%; 30-Year: 6.25% - 7.25% | 6.94% (ARMs) / 7.05% (fixed) | From 8.25% | Negotiable |

| Repayment Term | 15 or 30 Years | 15 or 30 Years | 3/1 ARM, 5/1 ARM, 7/1 ARM, or 30-year fixed | 6-18 Months | Negotiable (usually a balloon) |

| Time to Funding | 30-60 Days | 30-60 Days | 10-30 Days | 7-30 Days | Negotiable |

| Loan Limits | $50,000 - $1,867,274 (multifamily) | $50,000 - $1,867,274 (multifamily) | $75,000 - $2M | $75,000 - $2M | Negotiable |

| Report to Credit Bureaus? | Yes | Yes | No | No | No |

| Where to Apply | Try Credible | Try Credible | Try Kiavi, Visio, or Forman Loans | Try Kiavi, Forman Loans, Civic, or New Silver | N/A |

Final Thoughts on When To Refinance Rental Property

A good loan is a low-interest, fixed-rate mortgage for a term (15-30 years) that is appropriate for your financial goals.

But what if you bought an investment property with a bad loan? A high-interest loan or an adjustable-rate mortgage that just spiked? Then, and only then, it might make sense to refinance.

Still, you’ll need to look closely at how long your monthly savings will take to justify the cost and how much longer you’re extending your debt.

Remember that loan officers are salespeople. They are trying to sell you something — in this case, more debt.

Like nuclear reactors, debt can be a useful tool but also extremely dangerous. Always aim to get the right mortgage when you first purchase because refinancing later is very expensive.♦

What factors are influencing whether you refinance a rental property or take a different route?

Leaders Are Readers, So Keep Reading!

*Credible Disclosure: Prequalified rates are based on the information you provide and a soft credit inquiry. Receiving prequalified rates does not guarantee that the Lender will extend you an offer of credit. You are not yet approved for a loan or a specific rate. All credit decisions, including loan approval, if any, are determined by Lenders, in their sole discretion. Rates and terms are subject to change without notice. Rates from Lenders may differ from prequalified rates due to factors which may include, but are not limited to: (i) changes in your personal credit circumstances; (ii) additional information in your hard credit pull and/or additional information you provide (or are unable to provide) to the Lender during the underwriting process; and/or (iii) changes in APRs (e.g., an increase in the rate index between the time of prequalification and the time of application or loan closing. (Or, if the loan option is a variable rate loan, then the interest rate index used to set the APR is subject to increases or decreases at any time). Lenders reserve the right to change or withdraw the prequalified rates at any time.

Credible Operations, Inc. NMLS# 1681276, “Credible.” Not available in all states. www.nmlsconsumeraccess.org.

Connect with us on social!

What about the Brrrr method? When is a good time to refi then?

Hey Marie, with the BRRRR method you want to refinance for a permanent mortgage as soon as the renovations are complete. Here’s a detailed breakdown of the BRRRR strategy: https://sparkrental.com/brrrr-method-real-estate-leverage/.

Keep us posted on how we can help!

Remember that loan officers are salespeople trying to sell you something. That should put you in the right skeptical state of mind when they start making you offers.

Agreed Joe!

Great timing to read your article. I’ve started getting letters from my mortgage lender asking if I’m interested in a cash-out refi, and I confess I’ve thought about it. Thanks for sharing!

Glad to hear the article was helpful Fara!

Loan amortization is something every real estate investor needs to understand. Look at a full amortization table for any loan before moving forward with it.

Absolutely Pete!

Added some much-needed perspective on this. Thanks!

Glad to hear it was helpful Anya!