Take one look at an amortization schedule and you discover that “simple interest amortization” is a misnomer.

Still, it’s not rocket science either. An amortization table shows you how quickly you’ll pay down your loan balance over the course of your loan term. And you use the same amortization schedule calculator for mortgage loans, auto loans, student loans, personal loans, or any other installment loan.

Here’s how it works — and a free loan calculator with an amortization schedule.

Mortgage Loan Calculator with Amortization Schedule

Here’s the amortization schedule calculator for mortgages. This free online mortgage calculator amortization table can be adapted for various types of loans.

Start fiddling and diddling until you’re satisfied:

(article continues below)

Note: This mortgage calculator shows the monthly principal and interest payment, but doesn’t include mortgage insurance, homeowners insurance (or landlord insurance), property taxes, homeowners association fees, or other costs of owning a property.

As you can see, higher interest rates make a huge difference in how quickly you pay down your loan. The higher the interest rate, the longer you have to wait before seeing real progress in paying off your loan.

Unless, of course, you make extra mortgage payments.

What Is Amortization?

With a fixed-interest loan, your monthly payment remains the same for the entire life of the loan. This principle applies to all types of loans, including seller finance amortization schedules and auto loans. But that doesn’t mean each payment puts the same amount toward paying down your principal balance.

Speaking of which, you can use a car amortization schedule with extra payments or an auto loan amortization spreadsheet to plan your vehicle loan payments.

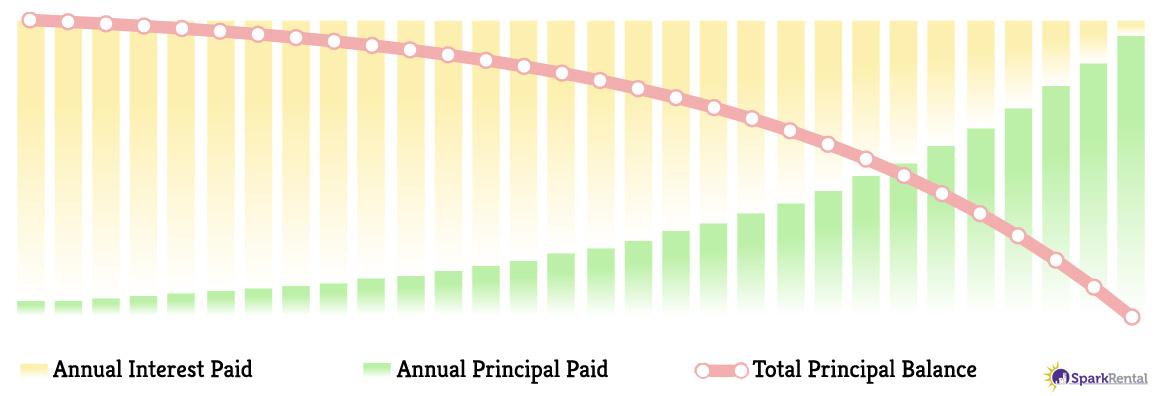

At the beginning of your loan, the bulk of each monthly payment goes toward interest. Over time, that proportion changes, with more of your monthly payment gradually going toward principal and less toward interest. Here’s an example amortization chart showing how your principal payment and balance changes over the life of the loan:

Lenders structure loans this way so that they collect plenty of interest up front. Often, you don’t start really paying off your outstanding balance until the last few years of your loan. The better to profit off you, my dear.

Lenders structure loans this way so that they collect plenty of interest up front. Often, you don’t start really paying off your outstanding balance until the last few years of your loan. The better to profit off you, my dear.

It also incentivizes them to refinance you before your loan gets to that point. They get to charge you a bunch of fresh fees and closing costs, and restart your amortization schedule from scratch, with most of each monthly payment going toward interest again.

Banks keep pulling that same trick every five years or so, always trying to keep you in the initial high-interest phase of the loan. It’s why they offer to roll closing costs into your loan when they refinance you!

Home mortgage lenders do it, rental property lenders do it, car lenders do it, every lender does it. It’s the oldest trick in the book, and you shouldn’t fall for it.

How Is an Amortization Schedule Calculated?

In an amortization schedule calculator for mortgage loans, you enter the loan amount, interest rate, and repayment term. The amortization calculator then spits out your monthly payment amount, but more importantly, it lists every single monthly payment for the entire life of your loan.

For each payment in the amortization schedule, it shows you how much of the payment goes toward interest, how much toward principal, and your remaining principal balance.

An amortization calculator for extra payments also gives you the option to include extra each month, and pay down your loan faster. Our amortization schedule calculator below includes this option. It helps you figure out how much extra you’ll need to pay each month to, say, pay off your 30-year loan amortization in 20 years.

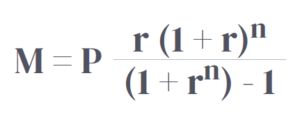

If you’re a math nerd, here’s the formula to calculate the monthly payment of a fixed-rate loan:

The variables break down as follows:

M: The total monthly loan payment.

P: The original loan amount.

r: Monthly interest rate (the annual interest rate divided by 12, so a 6% interest rate would be .06 / 12 = .005.

n: Total number of payments over the loan term, so a 15-year loan amortization or mortgage would have 180 monthly payments.

This same formula answers the question: how do you calculate seller financing? Tip: You can use a seller financing spreadsheet or mortgage calculator to run these numbers easily!

Ditch Your Day Job: How to Retire Early with Rental Income (Free 8-Video Course)

How Extra Payments Change Your Amortization Schedule

Making additional payments can help you escape the early high-interest phase of your amortization table much faster.

For example, if you borrow a $200,000 loan at 7% interest for 30 years, and you pay just $100 extra each month, you can knock out the loan in around 24 years instead of 30. Instead of paying $279,016 in interest, you pay $215,709 — a savings of $63,307.

Play around with the amortization calculator with extra payments to get a sense for how quickly you can pay down your loan. For some creative ideas, read up on ways to pay down your mortgage faster (including one that won’t impact your budget).

For more complex arrangements, such as owner financing, you may need an owner financing calculator with balloon payment options to plan your payments accurately.

Just make sure you don’t pay down your loan so fast that the lender hits you with a prepayment penalty! Check your mortgage terms to see if it comes with one.

Shorter Loan Terms, Less Total Interest

The shorter your loan term, the less total interest you’ll pay. Period.

Longer loans let your lender stuff more interest into the first half of the amortization schedule.

Use the amortization schedule calculator to run the numbers on just how much extra interest you’ll pay if you choose a 15-year mortgage versus a 30-year mortgage, for example. You probably won’t like what you see.

Sure, shorter loan terms mean higher monthly mortgage payments and lower real estate cash flow. But if you run the numbers with a rental cash flow calculator and find you can still end up in the black each month, it can save you a ton on interest in the long term.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Today’s Mortgage Interest Rates

Wondering how much interest you’re likely to pay for a mortgage in today’s market?

You can check this month’s interest rates for investment property loans; here’s the average interest rate on a 30-year home loan currently (compare quotes at Credible):

Whether you like what you see or not, here’s a word to the wise: don’t try to time the market. Interest rates could just as easily rise as fall, so holding out for lower interest rates might leave you stranded for years to come.

Of course, no one says you have to borrow money from a bank or mortgage lender. Try negotiating owner financing instead!

Alternatively, you can use revolving business lines of credit to fund your deals. Often they come with introductory 0% APR periods for the first 12-18 months. Check out this video explaining how it works.

Final Thoughts

A fixed monthly payment doesn’t mean that the same amount goes toward your principal balance each month. Expect to pay mostly interest at the beginning of your loan, and not make any real headway on paying down your balance until you near the end of it.

But that doesn’t mean you have to wait 30 years to pay off your mortgage loan. By making early payments, you can skip the worst of the initial interest. In fact, even making just one lump sum payment early in your amortization schedule can skip much of the early high-interest phase of your loan.

Play around with the amortization calculator for extra payments to see how quickly you can pay off your loan, and imagine how your cash flow will skyrocket once you pay off your mortgage.♦

Still have questions about mortgage amortization schedules or this loan amortization calculator? Wondering how your mortgage balance changes with one-time payments of extra funds? Fire questions at us below!

More Real Estate Investing Reads:

About the Author

G. Brian Davis is a landlord, real estate investor, and co-founder of SparkRental. His mission: to help 5,000 people reach financial independence by replacing their 9-5 jobs with rental income. If you want to be one of them, join Brian, Deni, and guest Scott Hoefler for a free masterclass on how Scott ditched his day job in under five years.

I want to know more about…

Connect with us on social!

Those who don’t understand how amortization is calculated are doomed to fall prey to lenders constantly pushing them to refinance. Great tool, thanks!

Amen Chester!

Oh man looking at that full amortization table brings home just how long a 30-year loan is. Thanks for the share!

Right?

Nice to see the entire loan payment schedule and balances laid out in a single chart. Thanks for the share!

Glad to hear it was helpful Jacob!

Thanks for sharing!

Absolutely Kevin!

I always found loan amortization confusing. Great simple explanation!

Thanks Ann Marie, glad it helped!

You need to understand how loans are structured if you want become an effective investor. At least if you plan on using financing, lol

Agreed Elizabeth!

I am going to sale one of rentals and carry the loan. Is there a calculator that I can download that will allow me to enter each month if the buyer pays more towards principal.

Hi Ronald, the loan amortization calculator above does have an option for extra payments. But I don’t have a loan calculator handy for you for managing one-off extra payments. I’m sure you can find one somewhere on the good ol’ interwebs though!