Cats or dogs? Coffee or tea? Real estate or stocks?

Age old questions. And while I’m a firm believer in both, sometimes you have to make a judgment call based on limited cash available to invest.

What performs the best over the long term? For that matter, where do bonds fit into the equation?

In a massive data analysis, economists from the University of California in Davis, the University of Bonn, and the Deutsche Bundesbank (Germany’s central bank) collaborated on an incredible new economic report titled “The Rate of Return on Everything” from 1870-2015.

Their findings, in a one-sentence summary? “Residential real estate, not equity, has been the best long-run investment over the course of modern history.”

If there’s ever a reason to believe in rental investing returns, this is it.

Here’s exactly what the study found, without getting too finance-geeky on you.

The Study

The five economists who collaborated on the study reviewed data from 16 wealthy, developed countries (listed further down). They compared the inflation-adjusted returns on short-term bills, long-term bonds, equities, and residential rental properties, from 1870-2015.

All forms of income for each asset class were included; both dividends and capital appreciation for stocks, both rental income and appreciation for real estate, etc. The economists also accounted for inflation in all asset returns.

In a nutshell, they found that residential rental properties boasted long-term returns of over 7%, while equities’ long-term returns fell under 7%. Bonds and bills lagged far behind both.

Digging Into the Details: Residential Real Estate vs. Equities

First, its worth noting that about half of the returns found in residential real estate came from rental income. The other half? From appreciation.

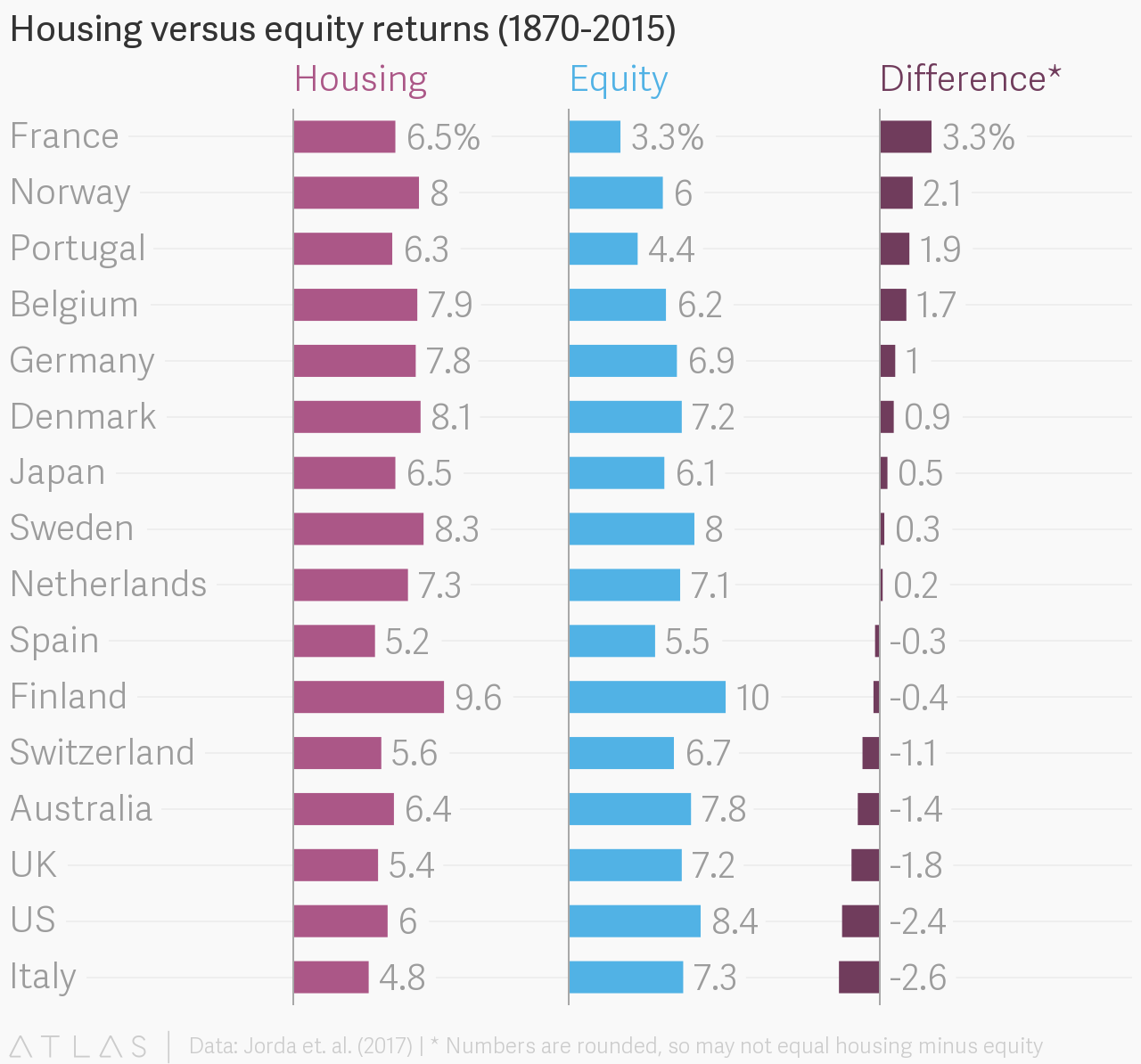

Not every country’s returns on rental properties or equities were identical, either. Here’s a breakdown of the 16 countries’ returns on residential real estate versus equities:

These returns have also shifted slightly over time, of course. Since 1980, equities have outperformed rental property returns; across the 16 countries, equity returns have averaged 10.7%, compared to 6.4% for rental real estate returns.

But before you go invest every penny in the stock market, it’s worth noting a few caveats. The researchers note that a few countries have skewed the total data, post-1980.

Specifically, Japan’s real estate collapse and Germany’s painfully slow residential real estate growth have skewed real estate returns lower, while equities experienced explosive growth in the Scandinavian countries of Finland, Norway, and Sweden.

And here’s the big game-changer, for the remaining skeptics: when the researchers adjusted for risk, rental properties’ returns still came out ahead of equities, even from 1980-2015.

Risk, Volatility, Real Estate & Equities

Here’s where things get interesting.

Historically, treasury bonds have been considered the safe, low-risk investment. Stocks meanwhile are far more volatile – they can shoot up in value quickly, then crash just as quickly the next year.

Thus, bonds have a reputation for being low-risk, low-return, while stocks are known for being high-risk, high-return. And deservedly so.

But residential rental properties? The new study shows in painstaking mathematical detail that rental properties are high-return, low-risk.

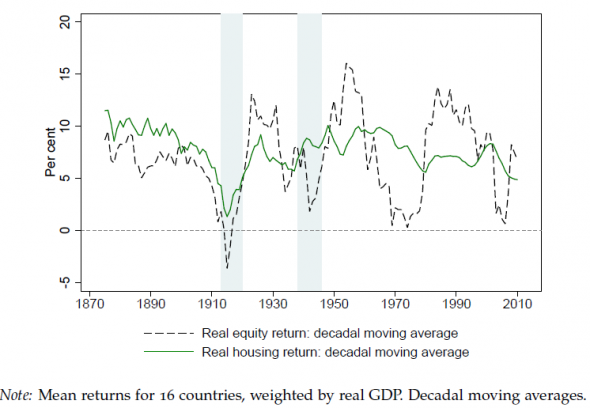

Just look at how much wider the swings in returns are for equities, compared to the relatively low-volatility returns on rental properties:

Chart courtesy of The Financial Times

That doesn’t make much sense, from an economics standpoint. An investment that offer high returns and low risk? Why isn’t everyone investing in them then?

I could throw some answers at you, like “The high barrier of entry from the capital required to buy real estate,” or “Real estate is not very liquid, so people are afraid to commit.” But the truth is, this new research has taken economists by surprise.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

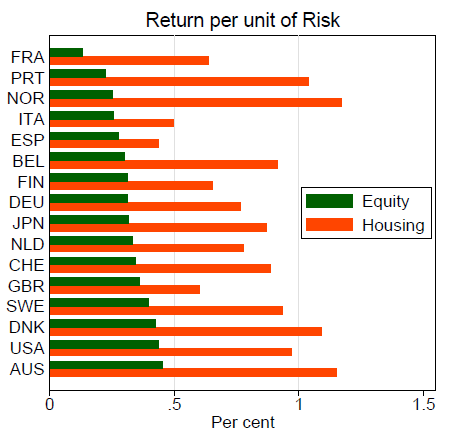

Sharpe Ratios to Measure Returns Over Risk

Let’s talk math for a second here. A common way of measuring risk vs. return for an investment is the Sharpe ratio: the ratio between the average annual return (above the short-term risk-free rate) and the risk/volatility, as measured by the annual standard deviation of the returns.

It’s literally a ratio of return over risk. So, a higher ratio means a better investment, for the risk.

Over the last 145 years, bonds have had a Sharpe ratio of around 0.2. Equities? Around 0.27. But residential rental properties? A whopping 0.7!

And since the 1950s, the Sharpe ratio for rental properties has been even higher, around 0.8.

Here’s a breakdown of each country, on the return per unit of risk:

Courtesy of the Financial Times

Returns vs. GDP Growth

How do returns in these advanced economies compare with growth in gross domestic product? Shouldn’t slow GDP growth hamper returns on equity and rental properties?

It turns out that returns on bonds, equities, and residential real estate don’t drag along the ground the way that GDP growth does, in first-world countries. Over the last 145 years, average returns (~6%) have actually risen at roughly double the pace of GDP growth (~3%).

Courtesy of The Economist

Since we’re big on visualization around here, see the graph to the right.

Interestingly, this also helps explain the growth of wealth inequality over time. Since it is primarily the better-off who own assets such as stocks and rental properties, they benefit from the faster growth of returns.

For those who do not invest, their income and net worth remain tied to the growth of the economy as a whole (i.e. GDP). They get a 3% raise as the economy improves, while those with investments see their wealth rise at twice the rate.

One more reason to save and invest as much of your money as possible, if you want to escape the rat race and reach financial independence!

What Does All This Say About Bonds?

I’ve expressed skepticism about bonds on numerous occasions, even when it comes to sequence risk and retiring early.

These low returns are exactly what I’m talking about.

Recently, a common refrain about bonds has been “Well sure, bonds haven’t performed well in the last 15 years, but that’s just temporary, with interest rates being so low. Look at how great bonds were in the ‘80s!”

Except it turns out that the ‘80s were the anomaly, not today. This long-term analysis of returns completely disproves the notion that bonds “normally” perform well, and that today’s markets are “abnormal.”

Bonds have even gone through extended periods, over the last 145 years, of generating negative returns!

In fact, this data calls into question the entire rationale behind investing in bonds. Above we touched on how bonds traditionally serve as a low-return, low-risk haven of those looking for safety. But why accept the pitifully low returns, when rental properties also provide low volatility and risk, but offer far better returns?

Rental properties serve a similar function: they create low-risk income. But they come with several advantages that bonds can’t boast.

First, they don’t expire. There’s no maturity date – they’re the gift that keeps on giving.

Then consider that rents rise alongside inflation, so you don’t have to subtract out inflation each year from your returns. It’s baked into your profits, as your rents rise even while your mortgage payment remains the same.

And then there’s that mortgage payment itself, which does expire. Sooner or later, you’ll get a huge boost in ROI and monthly rental cash flow.

Oh, and there’s that little issue that your rental property can’t declare bankruptcy. It’s a piece of physical property, and isn’t going anywhere. Even governments default on bonds sometimes!

All right, all right, around now is the time to acknowledge that rental income does come with fluctuations, as you need to make repairs, or a property turns over. Bond income is steady and predictable.

And low ROI.

Does This Mean I Should Stop Investing in Stocks?

Does This Mean I Should Stop Investing in Stocks?

In a word, no.

Equities and rental properties balance each other beautifully. Sure, stocks are volatile, and can drop by 30%, 40%, 50% or even more. But they also can skyrocket by 30% in a year. Look no further than how kind this decade has been to equity investors.

Like residential real estate, you can “flip” equities for a quick buck (AKA day trading). But for most of us, where equities really shine is long-term investing. They are truly passive income – no management required.

They’re also far more liquid than real estate; you can sell them on a moment’s notice, if an emergency rears its ugly head and you need cash today.

Investors can also diversify far more easily with stocks. You can put $100 in a small cap US mutual fund one moment, and put another $100 in a large cap Asian fund the next, and own equity in hundreds of companies across several hemispheres and market caps.

When it comes to reaching financial independence, investors might consider rental properties for building passive income for today, and stocks for building passive income in a decade or two. Over time, they’ll grow rich several times over through rental income, dividend income, asset appreciation, and the incredible tax advantages that come with rental properties and long-term capital gains!

What are your thoughts on this data? Are you rethinking your investment strategy at all? Don’t be shy!

Connect with us on social!

Wow! That’s some pretty surprising data. Fascinating though, how residential rental properties outperformed stocks, especially based on risk. Not surprising at all that bonds had such low returns though 🙂

I know Sally, right? I love this kind of nerding out!

…and this is why I’m a landlord. Great piece, thanks for bringing some data justifications to why we do what we do!

Why I’m a landlord too Maddie! Thanks for reading!

Hmm… interesting data. I wonder does it apply to developing countries, like in Indonesia, where I live.

Big proponent of real estate investing. I’ve got a few of my own properties as well as managing some properties for other people. I absolutely believe it outperforms when done correctly and it all aspects are considered. Nice data!

Thanks Ken, glad you found it useful!

The numbers can’t deny that rental property is the still best investment! Hooray to all landlords and real estate investors!

Amen Karen!

Having a vacation rental property was my childhood dream but my parents doesn’t support it. Now that they’re living in one of my rental units for free, I think it’s safe to say they’ve changed their mind about the power of rental investing.

Amen Illidan!