The Big Picture On FHA’s Kiddie Condo Loans:

-

- The FHA “Kiddie Condo” loans program allows for a down payment as low as 3.5%, making it an affordable option for parents co-signing a mortgage with their adult children.

- Parents can buy a property with their child, who lives in one unit while renting out the others, potentially covering mortgage costs and teaching property management skills.

- The program can be a strategic way to invest in real estate while also educating children about financial management and real estate investing.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

Have you ever wished you could borrow an FHA loan for a rental property without actually having to move into it?

For most real estate investors, coming up with a down payment for a rental property is the greatest barrier to buying. Most of us don’t just have $30,000 or $50,000 or $100,000 lying around collecting dust.

Typical rental property loans require at least 20% down in cash. And the down payment aside, the interest rates are higher than for owner-occupied mortgages.

But if you have adult children, you can capitalize on FHA’s “kiddie condo” loans to get FHA, owner-occupied financing for a rental property and potentially get the best condo mortgage rates.

“Kiddie Condo” Loans Overview

Now is a good time to mention that there’s no official FHA loan program called “Kiddie Condo.” That’s a term mortgage brokers invented as a marketing label.

Like many marketing labels, it has a nice ring, so we’re using it here.

Here’s the basic premise: FHA allows parents to co-sign their children’s mortgages as joint owners. (They also allow parents to co-sign without being on the deed, but that won’t serve your purposes here.)

In any event, parents can collaborate on real estate investments with their adult children. They can use FHA financing to fund the project if their children live on the property for at least a year.

For example, when my friend Tracy was in medical school, her parents bought a townhouse for her to live in. In turn, Tracy paid them rent, and years later, when she finished her residency, she moved away from Baltimore. Her parents had a rental property in excellent shape with strong equity.

Tracy’s parents financed it with a rental property loan. However, they could have borrowed an FHA mortgage if they had included Tracy in the deed.

“Kiddie Condo” Loans Requirements

Here’s an overview of the requirements for “Kiddie Condo” loans:

| Requirement | Details |

|---|---|

| Down Payment | Minimum 3.5% of the purchase price. |

| Credit Score | Typically, a minimum credit score of 580 is required. |

| Debt-to-Income Ratio | Generally, it is a maximum of 43%, but it can be higher with compensating factors. |

| Occupancy | At least one borrower must occupy the property as their primary residence. |

| Co-Borrower | Allowed, even if the co-borrower is not living in the property (e.g., parents co-signing). |

| Loan Limits | Subject to FHA loan limits, which vary by county and property type. |

| Mortgage Insurance | Required, including an upfront premium and annual premiums. |

| Property Types | It can be used for single-family homes, multi-family homes (up to 4 units), condos, and townhomes. |

House Hacking Through Your Children

In this way, parents can effectively house hack through their children. I’ve known parents who bought a property with their child; the child moved into one bedroom, and then they rented out the other bedrooms and/or units.

The child gets to live there for lower rent (or even for free), while the housemates pay enough rent to cover expenses. In exchange, the child handles property management: finding housemates, signing leases, collecting rent, handling repairs. This means they get real estate investing and property management experience in the bargain!

Meanwhile, the parents get an investment property, financed with cheap owner-occupied financing. And they don’t even have to pay a property manager.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

Advantages of FHA “Kiddie Condo” Loans House Hacking

I touched on some of the advantages above. Now, let’s go into a little more depth, before then walking through a few risks.

3.5% Down Payment

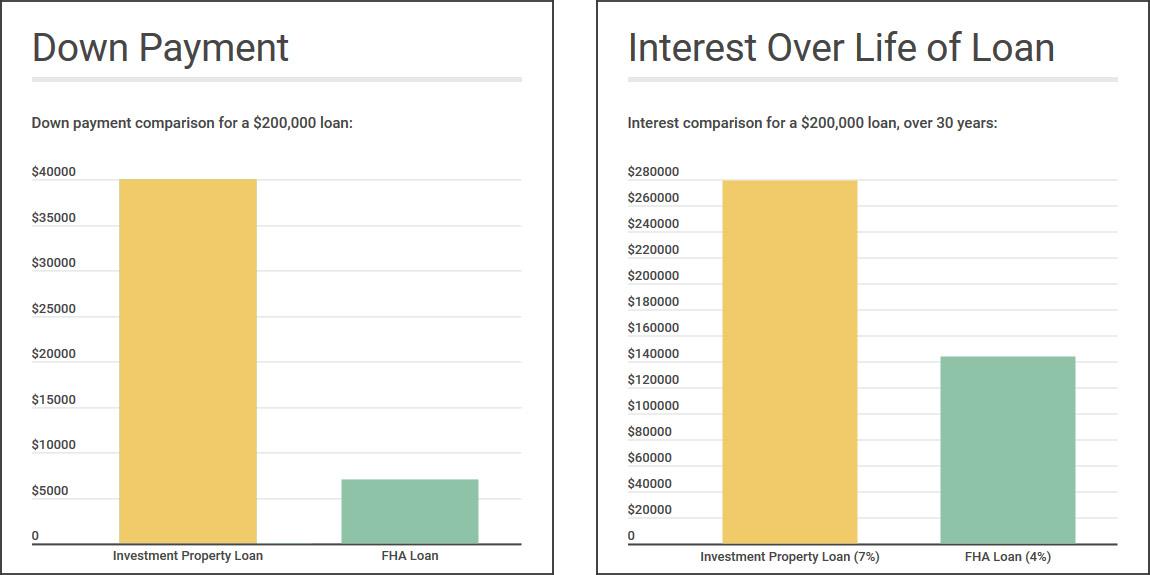

Borrowers with a credit score over 580 are eligible for an FHA loan with a mere 3.5% down. Even by homeowner loan standards, that’s low. For a down payment on a rental property, it’s unbelievable.

What about buying a condo with bad credit? Well, borrowers with rough credit in the 500-579 range can still qualify for an FHA loan with 10% down. To be frank, most borrowers with credit that low have no hope of borrowing any other type of mortgage, even portfolio rental property loans. (See the video at the bottom of the page for additional ideas for investing in real estate with bad credit.)

For a $200,000 rental property, most borrowers are looking at a $7,000 down payment for an FHA loan. Compare that to a (minimum!) $40,000 down payment through other types of rental property loans.

Low-Interest Rates & Fees

At the time of this writing, a reasonably strong borrower can expect to pay an FHA loan interest rate in the 4-4.5% range. A borrower with good credit can avoid paying points (a point is a one-time lender fee charged at settlement, equal to 1% of the loan amount). For instant prequalified interest rates and to compare different lenders’ terms, check out Credible*.

For portfolio rental property loans, borrowers are more likely to pay 5-8% plus 2-3 points.

The lifetime interest charged on a 30-year loan for $200,000 at 4% is $143,738.80. The same loan at 7% interest would cost $279,016.00 over the life of the loan. That’s nearly twice as much in interest.

Up to 4 Units

You might wonder, “Can I use FHA for investment property?” Well, buying a four-plex with an FHA loan is possible. This means you and your adult child can go in on a duplex, triplex, or fourplex, and they can move into one unit. You can rent out the other(s) to generate rental cash flow.

You can even use the theoretical income from these other units to help you qualify for the loan!

You Don’t Have to Live There

One drawback of house hacking a multifamily property is that you have to move into it yourself for at least one year after buying.

This poses several constraints. First, what if you don’t want to live in a multifamily property? Or what if you love your current home and don’t want to move anywhere?

Second, if you’re interested in building a rental portfolio, it restricts you to a maximum acquisition rate of one new rental property per year. And even then, conventional and FHA lenders will stop lending to you if you have more than two or three mortgages on your credit report.

By house-hacking kiddie-condo-style, you don’t have to move. Your child fulfills the owner-occupancy requirement for you, and even then, they’re only required to live there for one year.

Downsides to FHA Loans

FHA loans come with some persuasive advantages, but they are not all rainbows and butterflies. Before twisting your child’s arm into going in on a kiddie condo investment with you, here are some downsides worth considering.

Permanent MIP

Most mortgages allow owners to apply for mortgage insurance to be removed from the monthly payment once the loan balance drops below 80% of the property’s value.

Not so with FHA loans. Relatively recent changes to FHA loan specs require mortgage insurance to be paid for the entire life of the loan, often hundreds of extra dollars tacked onto your monthly payment.

Month after month, year after year, until you sell or refinance.

Reports on Your Credit

On the one hand, it’s a great way for your child to build a strong credit history early in adulthood.

At the same time, it may throw off your credit, even if you pay on time every month. Having higher debt balances can hurt your credit in the short term.

And, of course, it restricts your ability to borrow conventional mortgages on other rental properties.

If you want a private lender that doesn’t report on your credit, try Visio, LendingOne, or Patch Lending.

Not Scalable

As mentioned above, you can typically only have a few mortgages reporting on your credit before conventional and FHA lenders stop lending.

It’s also not scalable because it hinges on your child’s cooperation. And while a kiddie condo collaboration is a great way to go in on a deal with your kids in their 20s, don’t expect them to jump for joy when they’re 40 and you propose a kiddie house hacking deal to them.

Requires Responsible, Reliable Kiddos

It requires your kids’ cooperation, and they must also be responsible for caretaking the property.

They have to:

- Make the payment on time every month

- Collect rent on time from housemates and/or neighboring tenants

- Care for and protect the property from physical damage

- Enforce the lease agreement and potentially evict housemates or neighbors

Some 20-somethings aren’t up to those expectations. Know your children well before you propose a house-hacking project with them.

Tangled Personal & Financial Interests

What happens if your kid stops paying the rent or mortgage? If they trash the property?

You can’t evict someone if their name is on the deed.

This is a problem with any collaborative real estate investment between friends or family. If one party fails to live up to the agreement, the other party is up the proverbial creek.

And not only does it strain your finances, but it also strains your personal relationship. Even if your child lives up to their end of the agreement, things can still get hairy if their best friend is a housemate and tenant, and they stop paying the rent or trash the property.

Another challenge with going in on a rental property with someone else is that you need a mutually agreed-upon exit strategy. But when you’re buying as a long-term investment, there’s no obvious exit.

It happens all the time: one person decides they want to sell, and the other party is happy to keep collecting rents. This is fine if the one party can afford to buy the existing party out, but what happens if they can’t afford to do so?

These challenges aren’t necessarily deal-breakers, but they’re worth discussing before going in on a house hacking deal.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Teach Your Kids About Money & Investing (No One Else Will!)

They don’t teach personal finance, budgeting, investing, or real estate in public schools. This is probably why only 3% of Americans can answer five out of six questions accurately on a personal finance quiz.

If you want to arm your children with the financial and investing know-how they need to build long-term wealth, collaborating on a real estate investment with them is an excellent way to do it.

In fact, you should ideally start younger, with some of these tips to raise your kids to be good entrepreneurs rather than good employees. Employees are good at following orders; the entrepreneurial-minded are good at thinking strategically and taking charge of their financial future.

Teach your kids how to find good deals on real estate, secure a loan, and calculate rental cash flow. When you’re evaluating deals, sit down with them and use our rental income calculator together to show them how to calculate ROI!

Then come property management skills like collecting rent, showing vacant units, and filing evictions. Even better, if you’re handy and local, you can show them hands-on DIY property upgrades and home repairs.

Kids learn math, science, and grammar in school. They learn how to build wealth from you.

Opportunity to Invest in Long-Distance

As a final advantage to house hacking through your children, it opens the door to investing in long-distance real estate with local boots on the ground: your child.

If your kid attends college or grad school long-distance, they can offer some insights into the area. They can help you research up-and-coming areas, scope out promising neighborhoods, and serve as your eyes and ears.

Just be careful not to rely too heavily on their judgment: you’re the experienced investor, not them. And just because they like a ritzy neighborhood and want to live there doesn’t mean they can find a good return in that neighborhood.

Once you find a good deal, your child can oversee any (minor) repairs and, of course, take on increasing property management roles over time.

Final Word On FHA “Kiddie Condo” Loans

House hacking through your children, potentially with an FHA loan, can be a cheap, easy way to finance investment property. It’s also a great opportunity to teach your kids about real estate investing.

Agree on each party’s responsibilities and on an exit strategy, so you’re not locked into a real estate partnership indefinitely.

Most of all, make sure your child is responsible enough to partner with on a project worth hundreds of thousands of dollars. Not all 20-somethings make good business partners, so use good judgment about whether the broader concept is a good idea, before considering details like financing.

Would ever consider partnering with your child on a real estate investment? Why or why not?

Additional Tips for Investing in Real Estate with Bad Credit

More Creative Real Estate Investing Reads:

*Credible Disclosure: Prequalified rates are based on the information you provide and a soft credit inquiry. Receiving prequalified rates does not guarantee that the Lender will extend you an offer of credit. You are not yet approved for a loan or a specific rate. All credit decisions, including loan approval, if any, are determined by Lenders, in their sole discretion. Rates and terms are subject to change without notice. Rates from Lenders may differ from prequalified rates due to factors which may include, but are not limited to: (i) changes in your personal credit circumstances; (ii) additional information in your hard credit pull and/or additional information you provide (or are unable to provide) to the Lender during the underwriting process; and/or (iii) changes in APRs (e.g., an increase in the rate index between the time of prequalification and the time of application or loan closing. (Or, if the loan option is a variable rate loan, then the interest rate index used to set the APR is subject to increases or decreases at any time). Lenders reserve the right to change or withdraw the prequalified rates at any time.

Credible Operations, Inc. NMLS# 1681276, “Credible.” Not available in all states. www.nmlsconsumeraccess.org.

Connect with us on social!

Very cool idea! My daughter is 17 currently, something for us to consider when she goes off to college. Love this blog BTW, keep ’em coming!

Thanks Hank, much appreciated, and don’t worry, we will!

Something to definitely think about. Thank you for the information.

Thanks for the comment Deanne, and glad the article provided some food for thought!

Great Article that really has me thinking today! My oldest son just went off to college. He is staying at the dorms but this would be a great way to get him involved in real estate. I started investing in real estate the end of 2017 and I bought 5 Single famine homes in the last 16 months (my goal was 2 properties)! 🤦♂️ Brian Sr

Glad it was topical for you Brian! And congratulations on the rapid growth of your real estate portfolio!

Wow this is a wonderful information.. it would be very important to my daughter, shes in college. Thanks guys

Glad to hear it was useful for you Anne! Hope the two of you succeed in your first real estate investing partnership 🙂

Never thought to do this, but it’s a great idea. Thanks for the article, you guys always post creative stuff!

Appreciate it Jonathan, hope it works out well for you!

Great idea. We’re looking at buying a house for my son (and a couple of his friends) to live in because the dorms are so expensive. The kicker is, where do you find lenders who provide these “Kiddie Condo” mortgages? I keep running into places that only want to provide a conventional or secondary home loan at over 5% when rates on conventional are only 3%. (Credit score excellent and no loan payments at all right now.)

Hi Joyce, because your child is an owner-occupant, and you’re on the deed too as a buyer, many lenders will give you owner-occupant pricing. Keep talking to lenders, and explaining exactly how you’re structuring the deal. You should be able to find good pricing.

Do you have names of lender who do Kiddie Condo Loans? Also do they do them on non-warrantable condos?

Hi Glenda, these loans are a type of FHA loan, so check this database to see if the FHA will lend against the condo in question: https://entp.hud.gov/idapp/html/condlook.cfm?CFID=4813528&CFTOKEN=bd8d413066379740-3091D559-DDDB-DFAC-46C38378614E2767.

Does my child need to be on the deed.? Can she only be on the mortgage?

I believe lenders require the child to be on the deed alongside you as an owner, not just a cosigner for the mortgage, but you’ll have to speak with lenders about that.