The Big Picture On How To Become A Landlord:

-

- Rental properties can generate cash flow, appreciation, and tax benefits, but being a landlord requires some labor and expertise.

- If you just want to diversify into real estate and earn passive income, consider passive real estate investing instead.

- Landlords don’t earn as much cash flow as lay people think. Learn how to accurately calculate cash flow before even browsing rental properties.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

I love passive streams of income from real estate and property appreciation, for that matter. But before you learn how to become a landlord, you need to know exactly what you’re getting into.

Forget the cultural stereotypes about greedy, rich, lazy landlords. They’re not true. Becoming a landlord means taking on a real estate side hustle: you become a small business owner. It requires both labor and skill — and it takes time to learn those skills before you ever buy your first rental property.

Before making any offers on rental properties, make sure you understand the labor and skills required to become a landlord.

Active vs. Passive Real Estate Investing

First and foremost, ask yourself a simple question:

“Do I just want to diversify my portfolio to include real estate and earn passive income, or do I want to start a real estate investing business?”

If you just want sources of passive income and to diversify into real estate, there are easier ways to do it. By investing passively in real estate syndications or real estate crowdfunding. Consider real estate crowdfunding investments the “training wheels” of passive real estate investing. When you’re ready to level up, switch to passive real estate syndications.

To reiterate: you don’t need to become a landlord to get all the passive income, appreciation, and tax benefits of real estate investing. We aim for 15–30% returns on passive real estate investments in our Co-Investing Club. All investments include full tax benefits and then some, with accelerated depreciation.

If you have a passion for building your own real estate investing business, where you have total control over your assets — in exchange for working nights and weekends to build and manage that portfolio — then read on to learn how to become a landlord.

Things To Consider Before You Become A Landlord

Before you jump into the messy but rewarding world of real estate investing, you need to get a few very important things in line. Here are the questions you need to answer:

| Do you have a clear financial goal? | Do you want fast money? Or do you have the patience to wait years to get the return you want? Your investment decisions should always align with your active financial goals. Being a landlord is not the easy money most people think it is, so think carefully if you want to commit. |

| Have you done research on what tech you can use? | The internet is full of useful tools (including one of mine, which I’ll discuss later), some of which can be accessed on your phone. Leverage them to gain every advantage. |

| Have you talked to legal/financial professionals about your decisions? | Legal and financial experts might be expensive, but their advice can be a lifesaver, especially when you live in a region or state with complex regulations. |

| Are you willing to talk to people to build your network? | Some people might not be willing—or might not be able—to initiate rapport and handle the communication necessary to build their network. It’s a non-negotiable part of the deal, I’m afraid, so you’ll have to do it. |

How to Become a Landlord

I spent 15 years as a landlord and owned dozens of rental properties. Follow these steps to become a landlord with minimal risk and maximum returns.

1. Learn How Rental Cash Flow Works

Be honest: do you think that the cash flow on a rental property is just the rent minus the mortgage?

Before you ever even browse rental properties on real estate websites like Zillow, you need to know exactly how rental cash flow works. Otherwise, you’re about to enter a world of pain.

Landlords refer to a rule of thumb called the 50% Rule: you can expect around half of the rent to go to non-mortgage expenses. Those expenses include, but aren’t limited to:

-

- Vacancy rate

- Repairs and maintenance

- Property taxes

- Landlord insurance

- Property management fees (more on these momentarily)

- Accounting and bookkeeping costs

- Legal and marketing costs

Add them all up to average around 50% of the rent. And that’s before you talk about principal and interest on a rental property loan.

When new investors first learn about the 50% Rule, many scoff. “How am I ever supposed to find a property that cash flows well if half the rent goes out the window before even talking about the mortgage payment?”

How indeed. The answer: it’s a lot of work to find good deals. They’re not just sitting around the MLS, waiting for newbie investors to come along and start earning money from Day 1. Professional real estate investors go to great lengths to find deals, such as driving for dollars or digging through preforeclosure listings. Then they send out thousands of letters to those leads using direct mail campaigns.

The stark reality of becoming a landlord should be starting to come into focus.

Oh, and don’t dismiss property management costs by saying “I’ll just manage the property myself.” Property management is a labor expense, whether you do the labor or someone else does. Besides, the day will come when you are no longer willing or able to manage rental properties yourself anymore.

2. Choose a Market (and Learn Local Landlord Laws)

Here’s another wake up call: the city where you live may not be a good market for real estate investing. Mine certainly wasn’t.

Different cities and towns have different cap rates and gross rent multipliers (GRM). In some markets, like San Francisco, property prices cost far too much money compared to rents for landlords to reliably earn cash flow. Check out this interactive map of the best cities for real estate investing by GRM.

But price/rent ratios don’t tell you everything. Some markets impose extremely tenant-friendly laws, stacking the deck against property owners. I started my real estate investing career in Baltimore, MD, which has extremely antagonistic landlord-tenant laws.

Word to the wise: don’t invest in a market with anti-landlord laws. That goes for both the state and city levels of government.

If you decide to invest long-distance, prepare for extra challenges. It’s harder to network with all the support personnel you’ll need, from contractors to property managers to real estate agents. And it’s even harder to screen and vet them properly.

3. Choose a Strategy to Find Deals

3. Choose a Strategy to Find Deals

How do you plan to find properties that cash flow well? You can work with a realtor of course, but you’ll pay market value for any properties listed for sale on the MLS.

You could buy foreclosures or look into other ways to buy distressed properties. Tools like Propstream and Foreclosure.com make this easier, but you still need a systemized marketing plan to contact these owners. Check out our full Propstream review and Foreclosure.com review for more details; here’s a quick preview of how the latter works:

Or you could buy turnkey properties through an off-market turnkey seller, such as Norada Real Estate or Asset Column. You could browse turnkey properties on a marketplace like Roofstock.

Or perhaps you buy fixer-uppers and renovate them, to refinance and keep using the BRRRR strategy. Or any number of other strategies to find bargain deals.

Pick an investing strategy, any strategy, and learn everything you can about it from people who have actually done it.

4. Network with Lenders

Too many novice real estate investors start making offers before they have a plan for financing.

Sure, you could probably get away with using your home mortgage lender for your first investment property or two. But you can’t scale that way — to begin with, conventional mortgage loan programs have a cap on the number of mortgages allowed on your credit report.

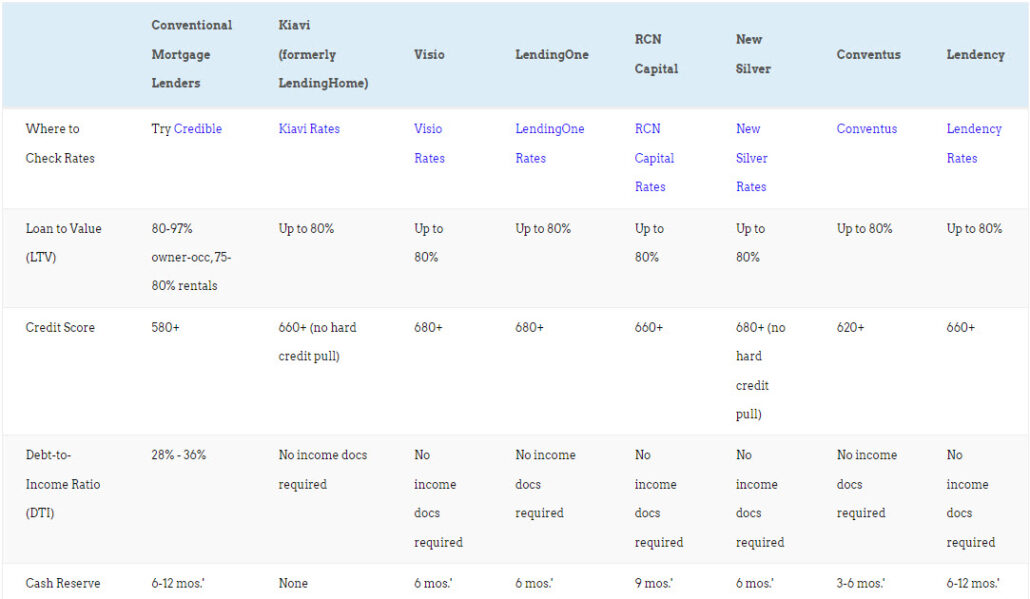

Start networking with portfolio lenders such as Kiavi, Visio, New Silver, and RCN Capital. The more loans you do with them, the better the loan terms they’ll offer you, and the more flexible their underwriting on your loans.

Portfolio lenders keep the loans in-house, in their own portfolio, rather than bundling them and selling them off like conventional mortgage lenders. Compare investment property loans and lenders for more options and information.

You can get more creative as well. For example, Fund&Grow helps you open up to $250,000 in unsecured business credit.

Start building your “financing toolkit” of options to fund real estate deals.

Real estate investments? Awesome. Being a landlord? Less fun.

Learn how to earn 15-30% on passive real estate investments in one free class.

5. Make Offers Based on Projected Cash Flow

You’re finally ready to start making offers. But before you put pen to paper (or finger to screen), run the numbers to calculate the cash flow. The last thing you want is to buy a liability that loses money each year, rather than an asset that earns it.

Fortunately, you don’t need fancy spreadsheets or a math degree. Use a free rental property calculator to forecast the cash flow for any property.

This requires you to research the rental market to accurately pinpoint the monthly rent.

Set a minimum annual yield, or cash-on-cash return, that you’re willing to accept. If a property doesn’t meet your minimum, don’t let sellers talk you into paying more and earning less.

6. Close on Your First Rental Property

A seller accepted your offer. Congratulations! Now what?

First, call your lender and submit a formal loan application. Note that portfolio lenders don’t look at your personal income, but rather analyze the debt service coverage ratio (DSCR) of any given property. They too want to make sure it’ll actually cash flow well.

If the property needs any repairs, start collecting quotes from contractors and handymen.

Always get a home inspection done. You don’t want any surprises.

At the closing table, you’ll sign the legal documents, pay a huge sum of money, and walk away the proud owner of a rental property.

7. Get the Property Move-In Ready

7. Get the Property Move-In Ready

Plan on sending in workers immediately to start on repairs. Every day the property sits vacant costs you money.

If the property was not previously in habitable condition, you may need to have it inspected by your local municipality. Once approved, they’ll issue a use and occupancy permit.

Depending on your local landlord-tenant laws, you may also need to register the property in a rental registry. And, of course, pay for the privilege.

You might even need to register it with the state. In Maryland, for example, landlords had to register their rental units with the Maryland Department of the Environment, and conduct lead paint inspections in between every single tenancy. And again, pay the fees for it.

8. Advertise Your Unit for Rent

As soon as you have attractive photos of the property, list it for rent and start showing it to prospective tenants.

Note that you may need to go beyond just advertising the unit the way you would think to look for homes. For example, if the rental property is in a heavily Hispanic neighborhood, you need to advertise it in Spanish, and potentially in offline venues. Do some research to see how your target tenants find homes, rather than assuming they find homes the same way you would.

Word to the wise: prescreen prospective renters before going all the way to the property to show it. There’s no point in wasting everyone’s time if the potential tenant isn’t a good fit for the property, due to insufficient income, pets, a low credit score, criminal background, or some other reason.

9. Screen Rental Applications

As you show the vacant unit, start collecting rental applications.

Some landlord softwares (cough cough) let you request tenant screening reports at the same time that you send the prospect the rental application. Just sayin’.

Don’t just get a tenant credit report and criminal background check; get an eviction history report, too. That gets to the heart of whether they’re a good tenant or not.

Think you’re done after reviewing the tenant screening reports? Think again. Now you need to pick up the phone and verify employment, income, and likelihood of continued employment. Ask their supervisor what kind of worker they are, how reliable and conscientious they are. Call their current landlord to ask about their rent payment history and how respectfully they treat their home. Then call up former landlords too, because current landlords might say anything to get rid of a bad tenant.

Tenant screening is arguably the most important task of being a landlord. The quality of your renters determines the quality of your returns. Period.

10. Sign a Lease Agreement

You’ve screened renters and found the perfect one. Now you draft and sign a rental agreement, AKA a lease contract or agreement.

Pay the money for a comprehensive, landlord-protective, state-specific lease agreement. Be cheap at your own peril here.

Check your local and state landlord-tenant laws to see if they require you to hold the security deposit in a specific type of account.

Set late fees and returned payment fees — and get ready to enforce them.

11. Collect Rents & Enforce Your Lease

New landlords inevitably fail to enforce their lease terms properly. They’ve been a renter for much of their lives, they’ve fallen for all those cultural stereotypes about mean landlords, so they buckle at the first sob story they hear from a tenant late on their rent.

Hear me well: people push boundaries. It’s human nature. Tenants will try and push your boundaries to see what you’ll let them get away with. If they can pay their rent two weeks late with no consequences, but their phone service stops working if they fail to pay on time, which bill do you think they’ll prioritize?

On the first of the month, send an automated email reminder. On the day before the rent officially becomes late, send a text or manual email reminding them that they’ll get hit with a late rent fee if you don’t receive the rent today.

When the rent officially becomes late, send an official eviction warning notice required by your state’s laws. Don’t freak out about it: they’ll still have ample time to bring the rent current. The eviction notice doesn’t say “get out” — it says “cure the violation or else I’ll file in rent court in X days.” You need to do this as soon as the courtesy period ends.

Don’t feel comfortable doing that like clockwork, every time? Don’t become a landlord. Invest in passive real estate syndications instead, or at the very least, hire a property manager.

12. Decide Whether to Hire a Property Manager

If you’re like most people, you’re busy. Do you really want to listen to tenant sob stories or field phone calls at 2 am when your renter clogs the toilet?

Consider delegating the day-to-day management to a property manager. Just beware that you’ll then have to manage the manager.

You’ll need to double check their tenant screening and selection, confirm how often they inspect the property, and make sure they’re serving eviction notices the day the rent officially becomes late.

A good property management company is worth their weight in gold. Unfortunately, the industry is rife with shoddy, unprofessional property managers.

Whether to hire a property manager isn’t always an easy decision. I’ve known real estate investors who actually hire the property manager first, before deciding to invest in a certain real estate market. Because without good property management, your returns will suffer, and an otherwise good property might lose money.

Pros & Cons of Becoming a Landlord

You now know how to become a landlord. But should you become a landlord?

Weigh the following pros and cons of becoming a landlord before committing your time and money.

Pros of Being a Landlord

I spent many years as a landlord, and it has a lot going for it. Consider the following upsides to owning rental property:

-

- Ongoing and expanding passive income: Once you buy a property, it continues paying passive income forever. In fact, that income grows over time, as rents rise even as your mortgage payments remain fixed.

- Appreciation: Even as you collect cash flow, your property also rises in value, at least in most cases.

- Leverage: You can buy real estate assets with other people’s money. A lender covers most of the cost, and your renters pay down your mortgage balance. Plus, your cash flow grows disproportionately faster than rents, since your mortgage payment stays the same even as rents go up.

- Tax benefits: Landlords enjoy dozens of rental property tax deductions. You don’t have to itemize your deductions, either — these come off your taxable rental income, so you can still take the standard deduction. Plus, you can deduct for depreciation and show a loss on your tax return even as you collect money in real life.

- Predictable cash flow: As outlined above, you can accurately forecast a property’s cash flow before buying. Once you master this, you can avoid bad investments moving forward.

Cons of Being a Landlord

Rental properties aren’t all fun and games. There’s a reason I sold off my rental properties, after all.

Beware of the following drawbacks before you become a landlord.

-

- High skill required: It takes knowledge to reliably make money on rental investments. And that knowledge requires dozens or more likely hundreds of hours to acquire.

- Not truly passive: Rental investing requires labor. Sure, we talk about “passive income,” but rental income isn’t actually passive. It requires work to find good deals on rental properties, work to line up financing and close on them, work to renovate them and rent them out and to manage them.

- Risk: Like all investments, rental properties come with risk. Risk that the tenant stops paying rent or destroys your property. Neighbors could also damage your property, or local “knuckleheads” (a euphemism if I’ve ever heard one) could vandalize it. There’s even a risk that the government will make lease agreements only one-way enforceable again, putting another eviction moratorium in place.

- Legal liability: Your tenants or neighbors or contractors can sue you. I’ve been sued twice as a landlord, and it sucks. Even when you win, you still lose, because it costs you money, time, and stress to defend yourself.

- Loan liability: When you borrow a rental property loan, you sign a personal guarantee. Fail to pay it back, and the lender can come after your personal assets such as your home, car, and baseball card collection.

FAQs About Becoming a Landlord

Still have a few questions about how to become a landlord?

Hopefully these will get you squared away.

Is becoming a landlord worth it?

It depends. If you have a passion for real estate and want to start a real estate side hustle as an investor and landlord, then absolutely. But if you just want to diversify your investment portfolio, there are much easier ways to do so. You can earn just as much (or more) passive income and appreciation from real estate syndications, or even real estate crowdfunding platforms, without the headaches.

Can you buy a rental property with no money down?

You can get creative with coming up with a down payment for a rental property. Theoretically you can buy a property with no money down. But that doesn’t mean it’s a good idea, as you might overleverage yourself and end up with negative cash flow.

Should I become a Section 8 landlord?

That’s a business decision you’ll have to make for yourself. On the plus side, Section 8 pays their portion of the rent on time every month. But the tenant doesn’t necessarily pay their portion on time (or at all). Worse, the annual inspection inevitably leaves you with thousands of dollars in repairs, which often aren’t necessary but writing up repairs is how Section 8 inspectors show their supervisors that they hit every property on their rounds.

Should I invest in local or long-distance rental properties?

It depends on whether your home city is a good market for rental investing. Many aren’t, in which case you have no choice but to look elsewhere if you want to invest in rental real estate.

Should I use the BRRRR method or buy turnkey rental properties?

If you invest long-distance, only buy turnkey properties. If you invest locally, you can consider buying fixer-uppers to follow the BRRRR strategy, but start small with cosmetic repairs. You add a whole new level of complications when you renovate properties.

Final Thoughts on Becoming a Landlord

First-time landlords tend to make the same handful of mistakes.

They underestimate operating expenses and overestimate rental cash flow. They lean too heavily on credit checks in the screening process, and don’t spend enough time checking on rental history with previous landlords or reliability with employers. And they don’t enforce their rental contracts when renters break the rules of the lease.

To be a successful landlord, you need to do better than other novices in the rental industry. Learn how to accurately budget for maintenance costs and major repairs, for vacancies and property damage. Aggressively stay on top of potential evictions — not because you enjoy it, but because you need to defend the boundaries of your lease to force good tenant behavior. Skip these expensive mistakes if you want to reliably earn positive cash flow.

Or skip them by investing passively in real estate instead.♦

What do you still want to know about how to become a landlord? What’s holding you back from becoming a landlord?

More Ideas to Help You Reach Financial Independence with Rentals!

Connect with us on social!

This is exactly what I want to do! Now I just need to convince my husband. He’s, shall we say, more “traditional”?

But I love that you guys do these types of in-depth stories about people who retired young with rental properties. Makes me glad I made the decision to become a landlord, even on the bad days when tenants are driving me nuts!

Make it happen Cara! Your husband will come around if you can find a way to inspire him. And I’m glad to hear you don’t regret your decision to become a landlord!

Oh, that sounds wonderful. Unfortunately, I have to work for a few more years

I hear you Chris! Hope you can take off sooner rather than later… let us know how we can help!

Great story Brian! Thought-provoking and inspiring. Very curious to hear the details of how they put their rental property in a self-directed IRA, looking forward to reading it

We’ll keep you updated Sally, and glad to hear you enjoyed their story!

Beautiful story and congrats on a life on the water.

I put a good chunk in the market now and up 12% during the last 12 months and keep a good chunk of cash. My point is like the last crash in the market, I pulled out early when I saw the signs and kept money out. I will the same the next one coming. There will be small losses but nothing that would wipe me out? Why don’t people just liquidate when they feel we are in a bear market or headed towards a financial meltdown? It’s not difficult to jump out and keep cash to use it somewhere else or stay on the sidelines.

Glad to hear you enjoyed it Mattej!

Personally I’m not big on trying to time the market – it’s rare when experts can agree on where we are in a market cycle, and if the experts don’t know, the rest of us will have a tough time too! But more power to you if you’ve had success in doing so.

Inspiring story Brian!

I’m looking forward to learning the details of the self directed IRA.

Thanks AR! It’s pretty fascinating, if you’re a money nerd like me!

you cannot buy european health insurance if you are not citizen

Also if you live the country more than 6 months you may lose ss benefits

There is more to this story then discussed here -numbers donot match

Saving 50% of earnings and spending half of what you earn is pretty amazing!

Agreed Mariko!

Love it!

Me too Kirk 🙂