The Big Picture On The Real Estate Cycle:

-

- Understanding the real estate market cycle is an important guide for informed investment decisions.

- Investors should focus on generating positive cash flow during recessions or uncertainties as a safer strategy, rather than relying on market appreciation.

- Using less leverage is recommended to minimize risk during market downturns, which allows investors to maintain stability and control over their investments.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

All markets are cyclical. As an investor, you need to understand the real estate cycle—or risk being a victim of the next real estate crash.

But that doesn’t mean you should try to time the market. Instead, just understand where we are in the housing market cycle at any given moment and how to protect yourself against future housing downturns.

The real estate market will dip, sooner or later, deeper or shallower. That leaves the question of how well you’ve prepared for the ups and downs of the real estate life cycle.

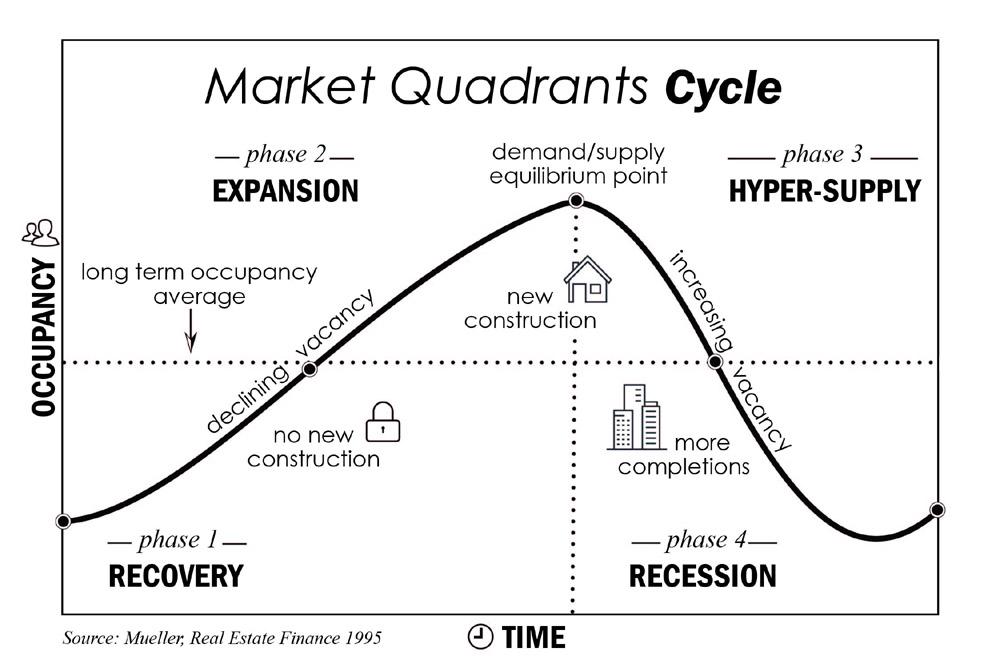

The Normal Real Estate Cycle

In a real estate crash, demand disappears even as supply continues growing. Because construction takes many months or even years to complete, it takes time for new supply to slow down to meet lower housing demand.

In point of fact, most investors are cautious these days, with investment volume going down 60% in Q2 2023.

Falling home prices spooked buyers and sellers alike, and the entire real estate industry contracted. But at a certain point, prices dropped low enough to spur demand again. Real estate prices level off and gradually start climbing again in the recovery phase.

Real estate values rise alongside demand, and then, as values rise, supply follows suit. Property owners increasingly grow tempted by high housing prices to list their homes for sale. Homebuilders gradually pick up the pace of construction until, once again, housing inventory starts outpacing demand. Eventually, a housing bubble can form when prices outpace local supply and demand.

Because it’s worth a thousand words, here’s a real estate cycle chart courtesy of Marshall Funding:

Notice that vacancies are the metric used to measure the balance between supply and demand. In your particular real estate market, pay close attention not just to the actual vacancy rate but also to the direction in which vacancies are trending. Decreasing vacancies indicate an upward-bound market while increasing vacancies represent a market poised to drop.

Finally, keep in mind that all housing markets are local. Often, different cities will be in different phases of the housing cycle and undergo real estate crashes at different times.

The Role of Interest Rates

When inflation runs too hot, or the economy appears to start overheating, central banks raise interest rates since most property buyers use financing, which raises the cost of buying real estate.

For example, a 30-year mortgage for $400,000 at 3% interest costs $1,686 monthly. At a 6% mortgage rate, the same loan costs $2,398 — over $700 more per month.

That means homebuyers (and investors, for that matter) just can’t afford to spend as much on properties. Demand dries up, which in turn pushes prices down.

Higher interest rates also make it harder for businesses to borrow money to grow and hire. This cools down the economy and can lead to a recession, which can further suppress property prices.

In recessions, the Federal Reserve lowers interest rates again, making it cheaper to buy real estate and spurring business growth. Which, of course, causes an expansion phase, and the real estate cycle continues.

Corrections Mean Opportunity

Real estate investors can make money at any phase of the housing market cycle. However, housing market crashes create an especially juicy opportunity.

Investors can buy at a discount when other buyers are huddling on the sidelines and gnashing their teeth about lower home values. Think of it as an occasional “sale” on real estate.

Nowadays, real estate investors lament, “It’s so much harder to find a good deal than it was in 2013!” But they forget how spooked most buyers and investors were in 2009-2013. After years of strong home value appreciation, it’s easy now to talk about how cheap real estate was back then. But most people were too scared to touch real estate at the time — and that’s why it was so cheap.

The next time prices drop in a housing market correction, consider investing instead instead of standing on the sidelines.

Protecting Against Real Estate Crashes

“It’s all well and good Brian to tell me to jump in and buy real estate when it’s just crashed, but how do I protect myself?”

Great question! I’m glad you asked. Starting today, here are five ways you can avoid losing money in the next real estate correction.

1. Invest Based on Today’s Cash Flow, Not Tomorrow’s Appreciation

In a real estate correction, home values drop. But rents may not drop at all — they sometimes rise!

When you buy real estate assuming that it will appreciate, you are speculating, not investing. Sure, the property may appreciate or plummet in value by 25%. You don’t know or have any control over the larger real estate market.

Instead, invest based on today’s rental cash flow. After running the numbers through a rental property calculator, are you satisfied with your cash flow and ROI? If the property temporarily drops in value but the rent stays the same, will you still be content with your investment?

If the answer is no, look for a property that offers better long-term cash flow.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

Rents Don’t Collapse

Rents are far, far more stable than home values over time. To illustrate this point, check out this graph charting the U.S. rent index since 2000, courtesy of the Federal Reserve:

Note that rental rates did flatline during the Great Recession. But they didn’t crash in the financial crisis like home prices did.

Housing values drop by far more in housing market corrections. Consider the following chart showing median U.S. home values since 2000:

One reason is that during real estate crashes, demand shifts from homebuying to renting. No one wants to buy a house when values are in freefall, so they rent instead. Renting is where people retreat when housing markets are in turmoil.

If you base your long-term rental investments based on today’s rents, there’s very little risk of a significant drop in rent. That doesn’t mean rents can’t fall — they can — but even when they do, they don’t fall like home values fall.

As a final chart, take a look at how rental vacancy rates moved since 2000:

Vacancy rates rose even as real estate values and rents rose throughout the 2000s, which defied the normal housing cycle. It was a warning that the housing market was abnormal.

Note that in the last eight years declining vacancies have mirrored rising rents and home values, as one expects in a normal housing market.

2. Buy Rent Default Insurance (or Make Your Renters Buy It)

To completely eliminate the risk of defaulted rent payments, you can insure against it. Insurance companies like The Guarantors and Steady offer rent default insurance, so if the tenant stops making payments, they pay the rent while you start the eviction process.

Many landlords have renters pay the annual premium on rent default insurance, which costs them nothing. If a rental application looks borderline, you can say, “While you wouldn’t ordinarily qualify to rent this unit, we can approve you if you agree to pay for a default rent insurance policy.” Some may balk, but you can sweeten the pot without a security deposit.

How? Because The Guarantors include damage protection in their rent default insurance policy.

3. Choose Low-Risk, High-Return Markets

No market is immune from real estate corrections. However, some markets are inherently riskier than others, and some markets are more likely to experience rent falls.

As we’ve discussed, this is the greatest threat to a long-term rental investor.

So, how can you tell which markets are at a higher risk for rents falling?

Before we analyze local markets, let’s pause to review what causes rents to decline. Rents fall for three main reasons:

- They were overpriced in a rent bubble,

- Demand falls and vacancies increase,

- Local unemployment rises and tenants lose their ability to pay the rent.

These are not mutually exclusive; one can cause another, or several can occur simultaneously.

As a real estate investor, your first goal must be to buy mathematically, based on research and data, not based on emotions. That sounds easy, but it’s too easy to fall in love with a property and then overpay or ignore warning signs.

Here are several ways to analyze markets, to buy in areas with a lower risk of falling rents in a housing market correction, and to avoid even looking at properties in riskier markets.

Check Real Estate Trends

Start with the most obvious: are rents and real estate values rising or falling?

An easy source for this data is Zillow. I’ll use Phoenix as an example since we recently did a co-investing joint venture in a real estate syndication there.

Just beware that skyrocketing prices and rents don’t necessarily signal continued growth. Once you get into double-digit appreciation, start worrying about unsustainable growth and a coming real estate market correction.

Review Historical Vacancy Rates

What’s today’s rental vacancy rate? More importantly, what direction is that vacancy rate trending?

For the top 75 metro areas in the US, the Census Bureau provides quarterly rental vacancy rates. Occupancy rates impact a real estate investment’s returns just as much as rent prices.

Beware of any market with rising vacancy rates.

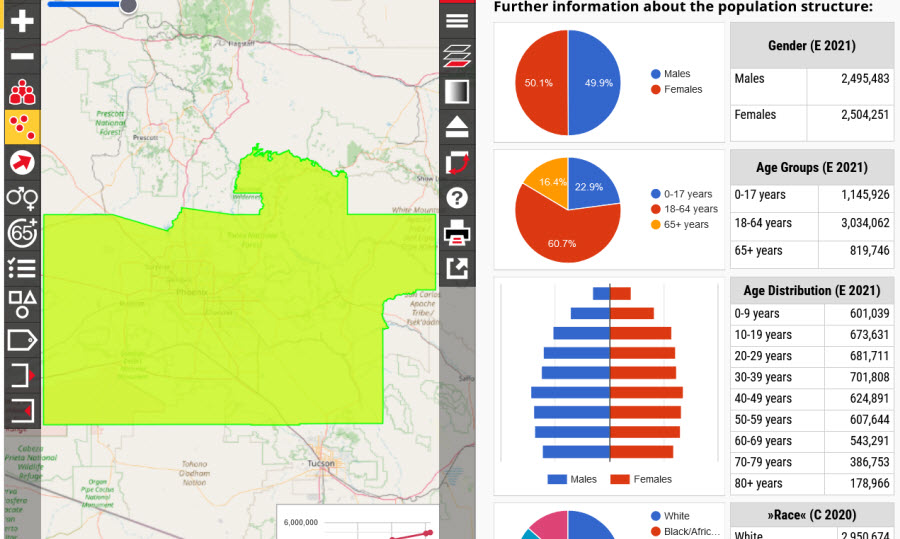

Check Population Trends

Is the population growing or shrinking? While there’s a niche in buying cheap properties in declining markets, it’s tricky and best left to specialist investors.

Buy properties in markets with growing populations. You can check population growth data on the Federal Reserve’s website:

Another measure to look at is the age distribution of the population. Growth markets tend to skew young, with plenty of kids and young adults. Young adults are more mobile and follow strong economies, whereas older adults are often the last to leave declining communities.

You can find age distribution data on CityPopulation.de:

Review the Economy

Once again, look not only at today’s economic growth and unemployment rate, but at which direction it’s trending.

For county-level data, once again the Federal Reserve offers a beautiful historical graph:

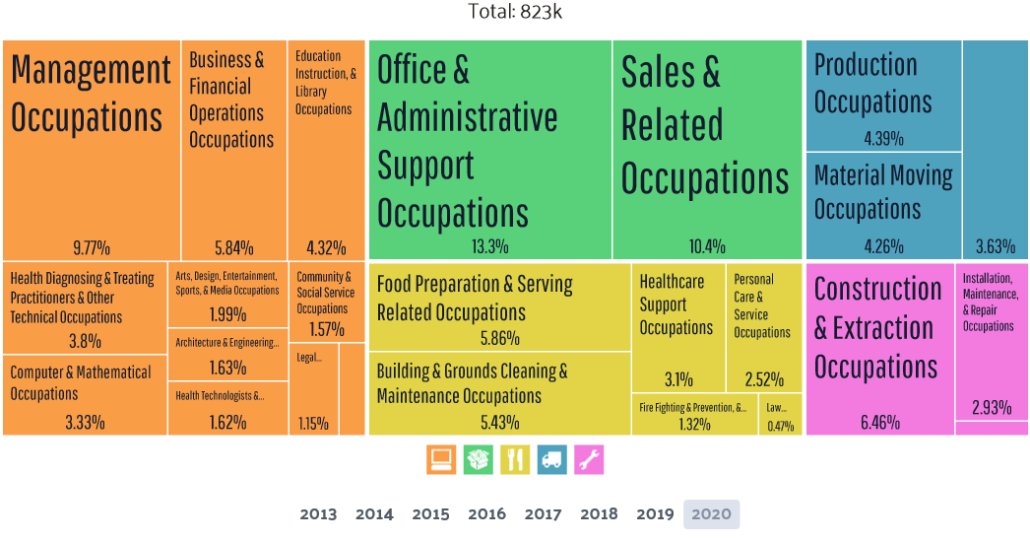

But the unemployment rate and job growth aren’t the only data to check. How diverse is the local economy? Coal mining towns didn’t do so well when coal mines shut down. The same goes for steel mill towns, or auto manufacturing towns (Flint Michigan, anyone?), or any other town over-dependent on a single industry.

To check the distribution of jobs across industries, try DataUSA.io:

4. Buy Properties with Room for Improvement

Another strategy to avoid losses during real estate market corrections is to buy properties where you can force appreciation. It leaves you the flexibility to either double-down and invest more money into ratcheting up the property’s appeal and asking rent, or leaving it as-is to keep it affordable in a correction.

You don’t want to own the best property in the neighborhood. You can improve your property, but you can’t easily improve the neighborhood.

Buying fixer-uppers leaves room for you to “force equity” by updating it and adding value.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

5. Less Leverage, Less Risk in a Housing Correction

I overleveraged myself in the lead-up to the last housing crisis. I borrowed the maximum possible loan amount on each property, crushing my cash flow and leaving me upside-down when housing values collapsed.

To protect yourself from a housing crash, lower your risk by using less real estate leverage. Instead of maxing out your loan at 85-90% LTV, consider 65-80%.

With a lower LTV (loan-to-value ratio), you’re less likely to become upside-down in a real estate downturn. You’re also far less likely to feel a cash flow pinch or experience negative cash flow.

Also be careful to avoid variable-interest loans or balloon mortgages. The last place you want to find yourself is forced to sell or refinance in the midst of a real estate correction, because your property will be worth far less. Refinancing is far more difficult during a housing correction, as home values drop and credit markets tighten.

Instead, borrow long-term fixed-interest mortgages for your rentals. Compare rental property loans here.

Another leverage-related strategy to lower your risk is to pay off one of your properties’ mortgages. With one less mortgage, your cash flow jumps, and it leaves you with a free-and-clear property that you can borrow against in an emergency.

6. Improve Your ROI with Better Property Management

Deni and I love to talk about the “Four Horsemen” of rental returns:

-

- Rent defaults & evictions

- Turnovers & vacancies

- Major repairs

- Lawsuits

Your job as a landlord is to minimize the risk of each. For example, you can minimize the risk of rent defaults and evictions with obsessively-thorough tenant screening. But it doesn’t end with running credit reports and eviction reports, or the likelihood of an applicant paying the rent on time.

Beyond tenant screening reports, you can minimize your turnover rate by screening for how long an applicant is likely to stay. How stable is their housing history? Do they have stable jobs? How long do they intend to stay? Are they willing to sign a multi-year lease agreement?

Speaking of lease agreements, you can use your lease to minimize the risk of damage and repairs. For examples, see these protective lease clauses.

You can also reduce your risk of rent defaults by collecting rent electronically. Here’s an overview in under 100 seconds of how you can automate your property management through an online landlord app like, say, SparkRental’s!

If you do nothing else, focus on only leasing to high-ROI tenants, on pruning your higher-risk and higher-headache tenants, and retaining your good tenants for as long as possible.

Surviving All Housing Market Cycles

Far too many real estate investors lose sleep during housing downturns. They see their equity dropping, and their net worth along with it.

First, remember that equity exists only on paper. It only becomes real upon sale. So? Don’t sell during a real estate market correction!

If your cash flow is strong, you can keep collecting rent and enjoying the passive income. No muss, no fuss. Your equity may have dropped, but who cares? You can ride out the real estate market cycle and watch it rise again.

There’s also some benefit with diversification. Different assets might be affected differently by market crashes. Some of them could drop faster, or possibly improve faster or higher. So, remember to diversify your investments across different neighborhoods, types of properties, sectors, and strategies.

Earlier, I mentioned how less leverage leads to lower risk in a real estate correction. Another way to lower your risk is liquidity.

The more money you have set aside in an emergency fund, the less exposed you are to any curveballs that could come your way in a recession or real estate downturn. You can withstand the occasional turnover, vacancy, or repair. With an adequate cash cushion, you don’t need to sell or borrow money if a big expense hits you.

Instead, you’re in a position to buy rental properties at a discount while everyone else is panicking about real estate.

Strategy Snapshot

Consider the most common real estate investment strategies here and their potential uses during specific market cycles.

| Phase of Real Estate Cycle | Strategy: Cash Flow Investing | Strategy: Appreciation Investing | Strategy: Fix and Flip |

|---|---|---|---|

| Expansion | Lower priority as prices rise, but stable properties can still generate steady income. | High potential for gains as property values increase rapidly. | Opportunities to renovate and sell quickly at higher prices. |

| Peak | Crucial for maintaining income as market tops out and prepares for potential downturn. | Risk increases as property prices may stagnate or fall. | Riskier if market turns quickly; timing and market knowledge critical. |

| Recession | Key strategy for stability, as properties with positive cash flow can weather lower property values. | Least favorable, as property values decrease. Potential long-term hold until recovery. | Market dependent; can be profitable if properties are acquired at low prices for future sale. |

| Recovery | Excellent time to acquire properties at lower costs to establish or increase cash flow before prices rise. | Good opportunity for long-term gains as the market begins to rise. | Very profitable if properties bought during the recession are renovated and sold as the market improves. |

Final Word

Housing market corrections are nothing to fear if you invest analytically and remain ready for a downturn at any time.

In fact, many real estate investors look forward to real estate crashes because they create fire-sale pricing on properties!

Investors who get in trouble during housing corrections are those who speculate on appreciation and overleverage themselves. If you invest based on today’s cash flow in growth markets with sound fundamentals, with leverage no higher than 80% LTV, you’ll be well positioned when the next real estate correction comes around.

Let the economic cycle roll. You’ll be ready for the next recession phase when it hits, whether tomorrow or in ten years.

What have your experiences been, with real estate market corrections?

More Awesome Real Estate Reads:

I want to know more about…

Connect with us on social!

Very comprehensive article, thanks. This is something I’ve been worried about for the last six months or so, truth be told. Glad to see I’m not the only one thinking about it, and that it’s not the “end of the world” that I had started thinking of it as.

You’re definitely not the only one thinking about housing corrections David! But the more you understand housing cycles the less scary the thought of a housing correction is.

Thank you Brian for your great article. I have positioned myself well. My last home I purchased for my future retirement. It has a suite which I did not rent, I enjoy. The rent from the main house pays 3/4 of the mortgage. I borrowed $16000 from my mother and $10,000 from my pension. I will have both paid off by January. I am thinking of taking a cash-out refinance on another home that I have no mortgage on, for three reasons: 1. Have money in the bank to enjoy. 2. Rates are so low that $200,000 mortgage will only cost me a little over $900 a month. I will still cashflow on this home by $1000 a month. 3. I would have a down payment for my next adventure. Should I cash out refinance on this home I have no mortgage on?

Congratulations on both house hacking successfully and the paid off property Nancy!

I would only cash out that property as part of a strategic plan to build your portfolio and earn more monthly cash flow. Run the numbers and see how they look. I wouldn’t use the cash out for personal spending though, just new investments.

Keep me posted Nancy!

Great article! Love how you walk us through everything! And specially how you’re nipping nonsense concerns with actual tangible empowering step with tips and tools. Like actually links to companies that offer Rent Default Insurance has been so so helpful, to lease tips. Many people say don’t worry without sharing it’s because they have options, or steps they can take to feel less worried. Thanks for sharing tangible steps to take!!

So glad you found it useful Diana!

Very well said. When I first started in real estate all I could afford was a home that I bought for $30k and put about $10k of work into it. I don’t think I ever made money on it and in the end I sold the headache for $25k. Purchase in good areas for cash flow and you should be just fine.

Thanks Abreu! I’m sorry you went through that initial experience, but I’ve had similar experiences with lower-end rental properties. Not fun.

This has been worrisome for quite a while now but it helps to keep a long-term cyclical perspective like this. Still not happy about building material costs increasing though!

I’m with you Lester!

Don’t panic over warnings about upcoming recession, financial dilemma, and other scare tactics over the internet. Instead focus on learning how to invest through all phases of economic and recession cycles. Great overview of housing cycles, and a great reminder that it all follows a pattern we’ve seen again and again.

Thanks Mark!

All markets are cyclical. Before investing in any asset market, you always need to understand what drives those cycles.

So true Vladimir!

My first market downturn was a challenging experience for me. I learned firsthand why so many people invest for reliable cash flow, rather than trying to forecast appreciation.

I hear that Katherine!