Generally, the credit bureaus consider anything over 670 a good credit score.

If your score is 671 or higher, you’re doing fairly well. The best credit score and the highest credit score possible is 850 for both FICO® and VantageScore models. FICO considers a score between 800 and 850 to be “exceptional,” while VantageScore considers a score above 780 to be “excellent.” It’s possible to get an 850 credit score, but it’s tough to achieve.

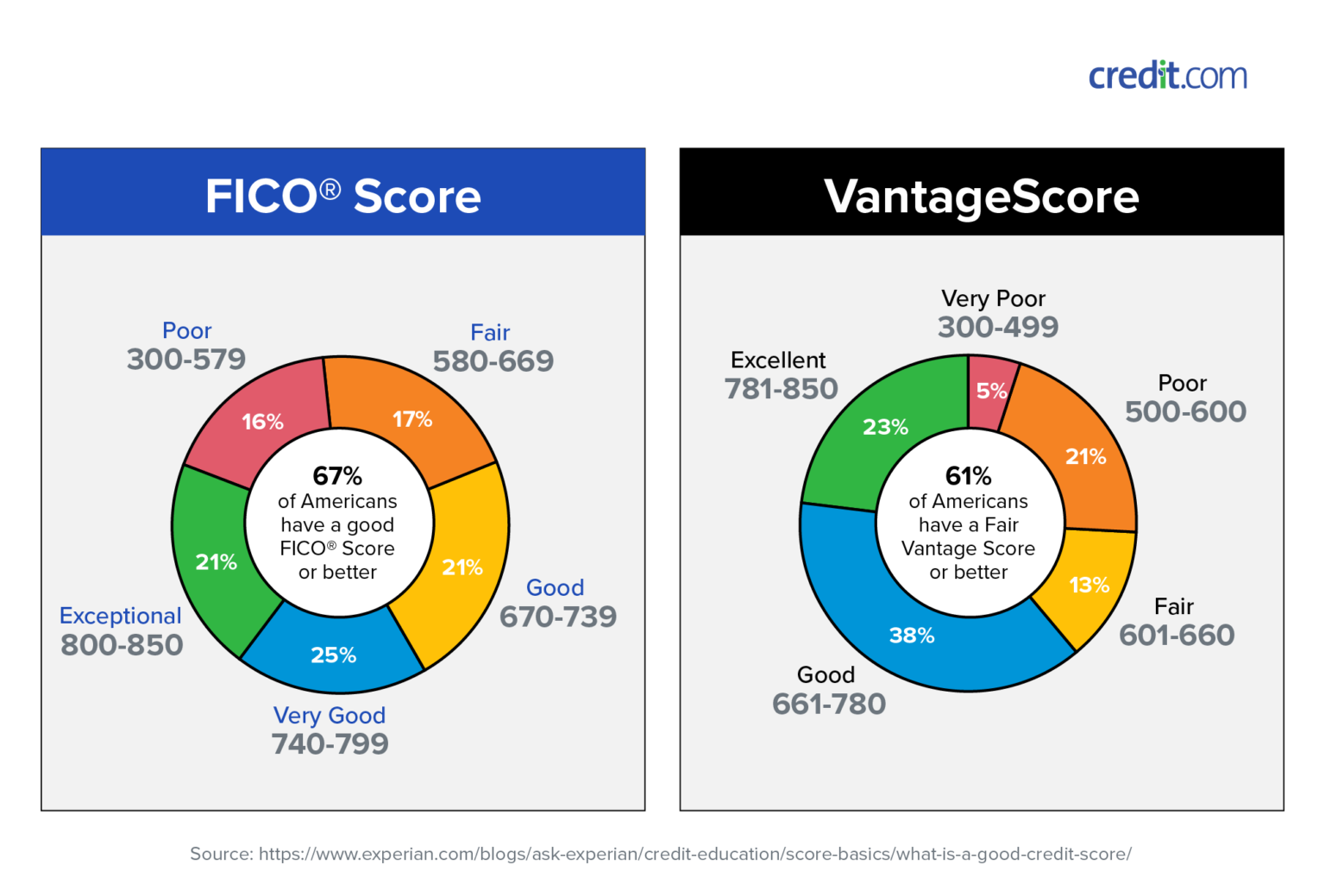

Credit Score Charts for FICO and VantageScore

Credit scores calculated using the FICO or VantageScore 3.0 scoring models range from 300 to 850. Those scores are broken down into five categories, though the breakdowns differ slightly.

For FICO, a good credit score is 670 or higher; a score above 800 is considered exceptional. For VantageScore 3.0, a good score is 661 or higher, and a score of 781 to 850 is excellent.

On the flip side, FICO scores below 670 fall into the fair and poor range, while VantageScore 3.0 scores below 660 are considered fair, poor, or very poor.

FICO and VantageScore aren’t the only credit scoring models. However, they are the most commonly used models and the ones used by the three major credit bureaus: Experian, Equifax, and TransUnion. Some lenders even have their own scoring models. But most lenders and credit card companies use FICO scores or VantageScores.

What Do Credit Scores Mean?

The three-digit numbers called credit scores are how the scoring institutions break down your credit profile. That number is calculated based on the information in your credit report at a credit bureau. Each bureau has its own file, which explains why your score might differ from one scoring institution to the next. Your file is a picture of how you’ve used credit to date.

Your score and where it falls tells lenders and credit card issuers how likely you are to pay off a loan, pay off a credit card, make late payments, and default on payments. In other words, it tells them if you’re an acceptable risk and if they should approve you for a loan or credit card.

A low score doesn’t necessarily mean lenders won’t give you a loan or card. Instead, it can mean they do so at a higher interest rate and with inferior loan terms. In other words, to offset the risk you pose, they charge you more interest or a higher annual fee.

For example, if you’re buying a $300,000 house with a 30-year fixed mortgage and you have good credit, you can end up paying around $94,000 less for that house over the life of the loan than if you had bad credit. (That assumes a difference of 1.6 percentage points in the interest rate of the mortgage.)

Scores are also used by landlords, cell phone companies, and even employers to check how risky you are.

Do Lenders Prefer a Good VantageScore Score Over a Good FICO Credit Score?

Lenders don’t necessarily prefer one score over the other. It’s likely, though, that a given lender uses only one credit scoring institution.

FICO reports that 90% of the top US lenders use FICO scores when deciding whether to loan money to an applicant. On the other hand, VantageScore states that between July 2018 and June 2019, approximately 12.3 billion VantageScore credit scores were used.

(article continues below)

Ditch Your Day Job: How to Retire Early with Rental Income (Free 8-Video Course)

- It was developed by the three major credit bureaus to offer a model across all bureaus that’s more consistent than FICO.

- It calculates scores for more people by giving a score to people with a shorter credit history.

Both models are consistent enough that knowing where you stand in one gives you a reliable indication of your credit in general.

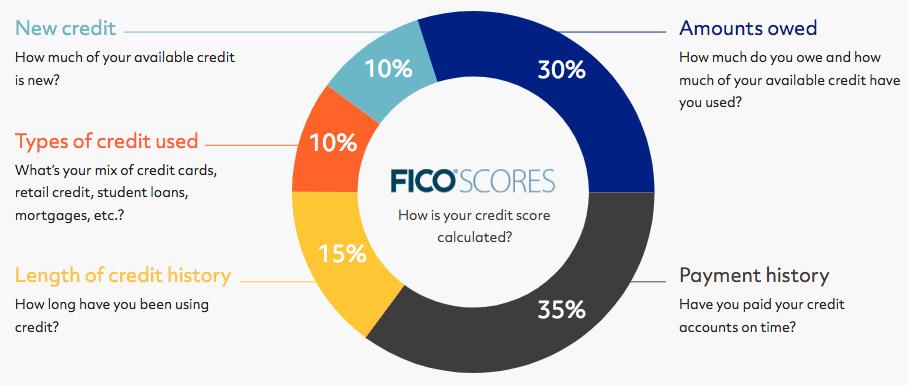

What Makes a Good Credit Score?

The same primary considerations go into calculating VantageScore credit scores and FICO credit scores:

-

- Payment history

- Credit utilization

- Credit age

- Mix of accounts

- New credit inquiries

Payment History

A history of late and missed payments for either scoring model lowers your credit score more than any other factor.

When determining your score, the FICO and VantageScore scoring models look at how recently you missed a payment or were late, how many accounts you were late on, and how many total payments on each account were missing or late.

Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’ve used divided by your total available credit limit. For example, if you have credit cards with a combined credit limit of $8,000 and balances of $3,000, your credit utilization ratio is 37.5%.

A good credit score requires a credit utilization ratio of 30% or less, although 10% or less is ideal.

Credit Age

Your credit age is how long you’ve used credit. More specifically, the length of your credit history is how long your credit accounts have been reported open, and your credit age is the average of how long all of your accounts have been open.

Say your oldest account was closed and fell off your file, and the next oldest account is 10 years “younger” than the account that fell off. Now, instead of showing how long you’ve actually used credit overall, credit files may show the age of the oldest account on file and your score may decrease.

To maintain a high credit age, keep at least one account on your credit file that is at least six months old. As you grow older, it should be easier to maintain a higher credit score as your accounts continue to grow in credit age.

Account Mix

Account mix is how many installment accounts and revolving accounts you have.

- Installment accounts are loans—such as mortgages, car loans, or personal loans—with a fixed monthly payment for a specific term (number of months or years).

- Revolving accounts are credit cards and credit lines with a credit limit that you can charge against.

Lenders want to see you can handle both types of accounts, so a good mix of the two makes for a better credit score.

Credit Inquiries

Hard inquiries happen when a lender looks at your credit report because you’ve applied for credit. A hard inquiry affects your credit score—lowering it by 5 to 10 points. The inquiry can stay on your credit report for up to two years, but it will impact your score for only 12 months. Though hard inquiries make up only 10% of your score, try to minimize credit inquiries to maximize your score.

When you need an auto loan or mortgage, it’s normal to shop around to find the best rates. Depending on the scoring model used, if you do your loan shopping in a 14- to 45-day span, the inquiries can be lumped into a single inquiry and affect your score less. FICO score models allow 45 days. On the other hand, the VantageScore model uses only a 14-day span.

Soft inquiries, such as SparkRental tenant credit reports use, don’t affect your credit score.

(article continues below)

Is a Credit Score the Only Thing Lenders Consider?

Lenders look at more than credit scores. The score plays a large factor, but so does your full credit report—sometimes from one bureau, sometimes from all three. Lenders may also look at your annual income and your debt-to-income ratio or overall debt.

Your debt-to-income ratio is calculated by dividing the total recurring monthly debt you have by your gross monthly income. This determines the percentage of debt you have compared to your income.

Credit card issuers and lenders may also look at how many reported delinquencies you have, how many hard inquiries were added to your credit file, your overall credit card utilization rate, your annual income, and your credit history’s health.

How Do I Get My Credit Scores?

You can get your full credit report from each credit bureau free once a year from AnnualCreditReport. Through April 2022, you can get a free copy of your credit report from each bureau weekly to help protect your financial health during the COVID-19 coronavirus pandemic. Those reports don’t include your credit score.

Most online options for viewing your credit score—free or paid—are limited to one or two scores. ExtraCredit from Credit.com takes it twenty-six steps further by offering you 28 of your FICO scores from all three major credit bureaus. When you sign up for an ExtraCredit account, you can also earn money when you get approved for select offers, monitor your accounts with $1 million identity theft insurance, and get exclusive discounts on credit repair services. All for one low monthly price.

If you’re not ready for ExtraCredit, Credit.com’s free Credit Report Card offers you your Experian VantageScore 3.0 credit score for free for life.

What if My Credit Score Is Less Than Good?

Now that you know what’s a good credit score, it’s crucial to act on yours. If your credit is fair or poor, find out why. Then you can address the factors and work to improve your credit score.

Do you need more credit history? Ask your landlord to start reporting your rents to the credit bureaus — a feature we offer with our online rent collection service.

You can also check out Credit.com’s ExtraCredit Build It feature. ExtraCredit identifies rent and utility bills you’re already paying and adds them to your credit profile as tradelines. This allows the credit bureaus to see additional payment information from you, which can help you build your credit profile.

This article originally appeared on Credit.com and is republished here with the author’s permission.

More on Credit & Financing:

About the Author

Credit.com is the only company of its kind to be founded and run by leading credit experts including journalists, authors and consumer advocates. We’re committed to helping consumers understand and master the confusing world of credit and improve their financial standing by recommending products and actions that are in their best interest.

I want to know more about…

Connect with us on social!

This is very informative and clearly explained. Thank you!

Glad it was helpful Sergio!

I think this should not be taken into account. Does credit score apply worldwide?

Credit scores are country-specific. To clarify, you disagree with the concept of people paying less for financing if they have a history of paying their bills on time?

Unfortunately, my credit score went a little bad because of unavoidable circumstances which results to some of my applications to be declined. Now, my plans are a little distorted and I am wondering if I can recover back in less than a year. Otherwise, I’m gonna try different avenue to get loans.

You may be able to rebuild your credit in a year – it just depends on what caused the damage in the first place. Keep making your payments on time, pay off your credit card balance in full every month, and you’ll rebuild credit.

Oh man, thanks for clearing my doubt! I always wondered if my credit score was bad.

Haha, I hope that means you now realize your credit is good, rather than confirming it’s bad!

I’ve been trying so hard for many years to improve my credit score but to no avail. Sometimes I have to back out because I can’t place cash deposit. Anyway, thanks for the tips. It’s just a matter of time to salvage my credit score.

Keep at it Melan. Takes time!