The Big Picture on How Much To Save To Retire Quickly:

-

- Your savings rate and living expenses significantly influence how much you need to save for retirement. Lowering living expenses both boosts your savings rate and decreases your required nest egg.

- Focus on the number of years until retirement rather than age. Your savings plan should be tailored to your retirement timeline, not just your age.

- Our calculation shows the required savings rates for different retirement horizons, assuming a 10% annual return on investments and a 4% withdrawal rate in retirement.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

How much do you need to save to retire young?

It depends on how quickly you want to retire and your target budget in retirement. But regardless of your income or target retirement spending, you can follow the same chart for how much to save to retire in 5, 10, 15, or 20 years.

Here’s what you need to know along with a concrete savings rate percentage depending on your timeline.

Retirement Age vs. Horizon

People ask me all the time: “How much do I need to save to retire by 40?” Or 30, or 45, or 50, or whatever.

Which I can’t even begin to answer until I know how old they are. A 20-year-old looking to retire by 40 is a lot different than a 35-year-old looking to retire in five years.

So, the first order of business is throwing out the framework of retirement age. Instead, think in terms of retirement horizon — the number of years you want to retire within.

Because it doesn’t matter if you’re 30 or 50 if you plan to retire within the next ten years. What you need to know is the same either way: How much do I need to save to retire in ten years?

In-depth Differences Between Retirement Age vs. Horizon

If you need any more clarity, here’s a quick table to explain the concepts:

| Aspect | Retirement Age | Retirement Horizon |

|---|---|---|

| Definition | The specific age at which a person plans to stop working and enter retirement. | The period or length of time remaining until retirement. |

| Focus | A fixed point in time, usually based on chronological age. | A span of years or duration leading up to retirement. |

| Example | Planning to retire at age 65. | Planning to retire in a specified number of years from now. |

| Relevance | Determines eligibility for age-related benefits like Social Security. | Affects savings strategy and investment decisions. |

| Impact on Planning | Requires ensuring sufficient savings and income streams to last from the retirement age onward. | Requires adjusting current savi ngs rates to achieve retirement goals within the horizon. |

| Adjustment Factors | Health, job satisfaction, and financial readiness can influence the exact retirement age. | Market performance, income growth, and life changes can impact the retirement horizon. |

| Financial Planning | Focus on ensuring a steady income flow starting from a specific age. | Focus on accumulating adequate savings and investments before the retirement date. |

| Common Strategies | – Save specific multiples of annual salary by set ages. – Use retirement calculators based on desired retirement age. | – Determine annual savings rate needed to reach financial goals by retirement. – Use time-based investment strategies like target-date funds. |

Glad we cleared that up.

Savings Rate & Living Expenses

Your savings rate is the percentage of your net income that you save. Or, more specifically, that you put toward either savings, investments, or paying down debts early.

The rest of your net income goes toward your living expenses.

Imagine you earn $6,000 per month before taxes, and $1,000 gets taken out for income taxes. Your remaining after-tax income of $5,000 per month is what you have to work with.

If you live on $4,000 per month and save the other $1,000 per month, your savings rate is 20%.

Note that your spending budget is a zero-sum game. If you spend more, it comes out of your savings rate. No matter what you spend or save, it all adds up to 100% of your net income.

How Much Do You Need to Save to Retire?

Here’s where it gets interesting: lower living expenses not only let you save more of your income now, but they also lower your target nest egg for retirement.

How much you need to save to retire doesn’t depend on your current income. It depends on how much money you need each month to cover your living expenses.

So, the lower your living expenses, the less you need to save to retire.

The classic rule for retirement savings is the 4% Rule: you can safely withdraw 4% of your retirement nest egg each year, with minimal risk of running out of money within 30 years.

That means that if you plan to live on $40,000 each year, you need $1 million saved for retirement.

In other words, you need to save 25 times your annual living expenses. The lower those living expenses, the less you need to save — by a factor of 25.

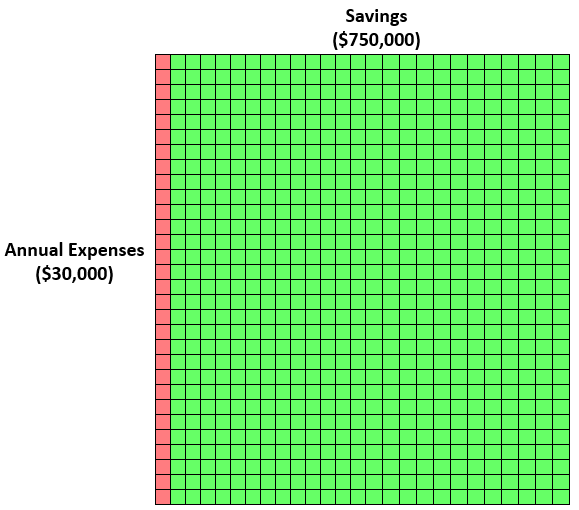

Zach from FourPillarFreedom illustrates this point well with tiny blocks. Each red block represents $1,000 in spending per year. Each green block shows how much you need to save to retire. Here’s how that looks, having to save $25 for every $1 of annual spending in retirement:

The point is simple: lowering your living expenses tackles the problem from two sides, both by boosting your savings rate (to build wealth faster) and lowering your target nest egg.

There are other ways to calculate how much you need to retire, like aiming to save 100% of your annual salary by 30, 300% by 40, and so on, or flat-out saving 25% of your salary throughout the years, but let’s focus on my and Zach’s method.

(article continues below)

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

How Much to Save to Retire: Charted

I ran the numbers of exactly how much money you need to save to retire within different time horizons.

Before diving into the chart, I made three assumptions to calculate how much to save for retirement. First, I assumed a 10% annual return on your investments. If that seems high, consider that the historical stock market return is around 10.5% per year for the S&P 500. You can also earn higher cash-on-cash returns on rental properties, using leverage in real estate investments.

The second assumption was a 4% withdrawal rate in retirement (the 4% Rule). But with rental properties, you can bend that rule using tactics like the BRRRR method.

Finally, I assumed that you maintain the same living expenses in retirement that you have while working. So, if you earn $5,000 in after-tax income, and have a savings rate of 20%, that assumes that you continue spending $4,000 a month in retirement ($48,000 per year, which would require a $1.2 million nest egg if you follow the 4% rule of thumb).

Here’s the savings rate you need to retire at different time horizons:

| Savings Rate | Time (in Years) |

| 5% | 40.8 |

| 10% | 33.2 |

| 15% | 28.6 |

| 20% | 25.2 |

| 25% | 22.5 |

| 30% | 20.2 |

| 40% | 16.4 |

| 50% | 13.2 |

| 60% | 10.3 |

| 70% | 7.7 |

| 80% | 5.1 |

Specific Example

To illustrate those numbers with an example, say your after-tax annual income is $100,000 ($8,333.33/month). Your monthly savings, target monthly spending, and target nest egg would look like this for different savings rates:

| Savings Rate | Monthly Savings | Monthly Living Expenses | Target Annual Income | Target Nest Egg | Years to Reach | ||||

|---|---|---|---|---|---|---|---|---|---|

| 5% | $416.67 | $7,916.67 | $95,000.00 | $2,375,000.00 | 40.8 | ||||

| 10% | $833.33 | $7,500.00 | $90,000.00 | $2,250,000.00 | 33.2 | ||||

| 15% | $1,250.00 | $7,083.33 | $85,000.00 | $2,125,000.00 | 28.6 | ||||

| 20% | $1,666.67 | $6,666.67 | $80,000.00 | $2,000,000.00 | 25.2 | ||||

| 25% | $2,083.33 | $6,250.00 | $75,000.00 | $1,875,000.00 | 22.5 | ||||

| 30% | $2,500.00 | $5,833.33 | $70,000.00 | $1,750,000.00 | 20.2 | ||||

| 40% | $3,333.33 | $5,000.00 | $60,000.00 | $1,500,000.00 | 16.4 | ||||

| 50% | $4,166.67 | $4,166.67 | $50,000.00 | $1,250,000.00 | 13.2 | ||||

| 60% | $5,000.00 | $3,333.33 | $40,000.00 | $1,000,000.00 | 10.3 | ||||

| 70% | $5,833.33 | $2,500.00 | $30,000.00 | $750,000.00 | 7.7 | ||||

| 80% | $6,666.67 | $1,666.67 | $20,000.00 | $500,000.00 | 5.1 |

Note that these figures don’t account for income taxes in retirement. But you do have plenty of options to reduce or avoid taxes in retirement, from Roth IRAs to rental property tax deductions to ways to avoid capital gains tax on real estate.

The above numbers also don’t account for Social Security benefits, which you may well receive. See our financial independence/early retirement calculator to include these and other sources of income such as rental properties.

These tables could use a bit more explanation though, so here are a few thoughts on reaching financial independence and early retirement (FIRE) on a fast timeline.

How Much to Save to Retire in 5 Years

Even with an 80% savings rate, it would still take just over five years to reach financial independence — at least with the assumptions built into this exercise.

In the example above, where you take home $8,333 per month, that means living on $1,667 per month. Not just now, but also in retirement.

That’s a tall order in today’s world.

If you want to retire in five years, you’re going to need to bend some rules. Plan on either earning a higher rate of return than the 10% I used to run these numbers or bend the 4% Rule by investing in real estate.

For example, if you can reuse the same down payment over and over by refinancing rental properties with the BRRRR method, you can theoretically reach financial freedom with a single down payment.

You can further bend the rules by continuing to work post-retirement, doing something fun or meaningful (ideally both). I like to imagine myself working part-time at a winery to bring in extra money in retirement, for example.

How Much to Save for Retirement in 10 Years

With a 60% savings rate, you can retire in ten years.

Continuing the example above, that would mean living on $3,333 per month, and investing the other $5,000 you earn each month. Millions of Americans live on a similar budget, but don’t expect to live in the lap of luxury.

Again, look for ways to bend the rules with higher investment returns, higher withdrawal rates, more leverage, or continuing to work part- or full-time doing something fun for post-retirement income. Take advantage of employer matching contributions to tax-advantaged retirement accounts. It’s effectively free money, helping you boost your savings rate and hit your savings goals faster.

How Much to Save to Retire in 15 Years

If you’re willing to save around 45% of your income, you can reach financial independence and retire in 15 years.

In the example above, that means saving $3,750 each month, and living on the other $4,583. We’re entering a more practical realm for the average person interested in financial independence and early retirement.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Planning for Inflation in Retirement

Contrary to popular belief, the 4% Rule does take inflation into account.

The rule dictates that the first year you retire, you withdraw 4% of your nest egg. Each year thereafter, you withdraw the same amount, adjusted upward for inflation (usually around 2%).

So, if you withdraw $40,000 of your $1,000,000 nest egg in the first year you retire, the next year you withdraw $40,800, assuming a 2% inflation rate. The year after that, you withdraw $41,616, and so forth.

Bear in mind, however, that real estate offers excellent protection against inflation. Rents don’t just rise alongside inflation — they’re one of the primary drivers of inflation. Consider it one more way that rental properties bend the rules in retirement planning.

Calculate How Much to Save for Retirement

Your next step is to calculate how much you need to save for retirement. To do that, start by answering a simple question: “How much income do I need in retirement?”

Some of your costs will likely decline in retirement, such as work clothes, work lunches, and commuting costs such as gas. Others might go up, such as travel expenses.

You don’t need to calculate your post-retirement spending to the penny. When in doubt, just use your current living expenses.

Multiply those annual living expenses by 25 to roughly calculate how much to save for retirement.

Again, the better you are at investing, the better your odds of bending the traditional retirement planning rules. You can potentially earn higher returns than the 10% average, especially if you learn how to use leverage in real estate investing. And reaching financial freedom at a young age gives you more flexibility to keep earning “post-retirement,” or even to go back to work full-time in a worst-case scenario.

All of which helps boost your risk tolerance, and pursue higher returns on investment.

Because real life is messy, and you’ll have multiple streams of income in retirement, check out our free financial independence calculator that takes rental income and post-retirement work into account, on top of paper assets and Social Security income.

The FIRE Lifestyle Before Reaching FIRE

The more passive income you earn from your investments, the less you need your day job to survive.

That frees you up to pursue work you’re more passionate about, a lifestyle you love regardless of the paycheck. My wife and I aren’t financially independent yet, but I already live the financially independent lifestyle. I get to manage a 100% remote business while living overseas with my wife and daughter. I set my own hours and we visit many countries each year.

We can do this because we live entirely on my wife’s income while investing all of mine. That leaves us with a savings rate of around 70% of our household income, and it all goes into compounding investments.

In other words, financial independence isn’t just about your retirement goals. When you start thinking in terms of financial independence, it frees you to think bigger about lifestyle design. And when you start focusing on designing your ideal lifestyle, it frees you to ditch your day job and start living the FIRE lifestyle before you reach financial independence.♦

How much money do you need to save to retire? How quickly are you aiming to reach financial independence and retire?

More Real Estate Investing Reads:

I want to know more about…

Connect with us on social!

I have a concern. If we are to assume that a person maintains the same living expenses in retirement, how do we account for inflation then?

The 4% Rule accounts for inflation – it’s only 4% of your net worth in the first year, then you adjust your withdrawals upward for inflation each year after that. Rental property returns also adjust for inflation, as you raise rents.

This means a lot! I saw a documentary video that warns us about the upcoming economic downfall and the best way to survive is to save money.

Absolutely – building up your savings and investments is one of the best ways to protect against future uncertainty.

This is an excellent topic to discuss. Many of us face such problems. We don’t know how much to save if we want to retire.

Very true Andy. Keep us posted on your progress!

Before, I was aiming $1M savings but I realized it’s not realistic so I lower it to 500k. In that way, I can start my first passive income while I am reaching my financial independence. It’s the best approach I can think of.

Just keep investing steadily each month Aileen and you’ll get there!

Well, in my opinion, you can’t figure out a number. You can’t really tell how much would you need when you retire. Can you?

If you don’t have a target, how do you know when you’ve hit it? But speaking to your broader question about uncertainty, that’s one reason I love the concept of financial independence at a young age: you can keep working and earning money post-FIRE, just doing something you love.