The Big Picture On Investing In Real Estate vs. Stocks:

-

- Real estate offers more control, predictability, and cash flow than stocks, especially for those looking to leverage assets. However, it demands more work, higher upfront costs, and lacks liquidity.

- Stocks are easy to diversify, liquid, and can be more passive than real estate. However, they are prone to volatility and sequence risk and offer less control over outcomes.

- A blended approach using real estate for income and stocks for growth can enhance financial independence (FI) and risk management. Balancing both offers stability and faster progress toward early retirement.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

Should you invest in real estate or stocks if you want to reach financial independence and/or retire early (FIRE) within the next five to ten years?

Both have advantages and disadvantages. Several US and German universities, along with the German central bank, even conducted an exhaustive study on real estate versus stocks to compare returns over the last 145 years.

The short version of their finding? Real estate had slightly higher returns and significantly lower volatility and risk. However, a deeper analysis proves less cut-and-dry, as stocks have outperformed real estate in the last 30 years.

If you’re looking for a fast track or retirement catch-up plan, here’s exactly what you need to know about real estate investing vs. the stock market – and how to capitalize on the strengths of each.

Advantages of Real Estate vs. Stocks

To help you decide between real estate or stocks for your early retirement plan, I’ll outline the advantages and disadvantages of both real estate investments and stocks. After explaining some pros and cons, I’ll break down some sample numbers for how your portfolio might look as you invest for passive income and FIRE.

Strap in!

Leverage

Real estate investors can typically borrow 80% of the purchase price with a rental property loan. In other words, they can buy an asset worth $100,000 with only $20,000; over time, their tenants will pay off the mortgage.

If they house hack by buying a small multifamily and moving into one of the units, they can borrow up to 96.5% of the purchase price with an FHA loan.

In fact, savvy investors can use the BRRRR strategy of real estate leverage to repeatedly recycle the same down payment money. It stands for buy, renovate, rent, refinance, repeat. When you refinance, you pull out your original down payment to reuse on the next property. Investors can keep reusing the same $30,000 to build a huge portfolio of rental properties in this way.

Stock investors can also take advantage of leverage but with far less flexibility. When stock investors buy on margin, they can typically borrow up to 50% of the cost to buy new stocks. Even then, if their portfolio balance falls, they’re subject to a “margin call” – the brokerage can force them to sell their stocks (at a huge loss) to recover the loan.

Score one for real estate versus stocks.

Real Estate vs Stock Market Leverage

Sure, leverage can amplify returns on investment capital, but the terms, flexibility, and risks vary between asset classes. Let’s take a closer look.

|

Leverage Comparison |

Real Estate |

Stocks |

|

Typical Down Payment |

20% (traditional) or 3.5% (FHA) |

50% (margin trading) |

|

Max Leverage Ratio |

Up to 27:1 (with FHA) |

2:1 |

|

Forced Sale Risk |

Very low (if payments made) |

High (margin calls) |

|

Interest Rates |

Generally lower, tax-deductible |

Higher, not tax-deductible |

|

Payment Source |

Tenants cover mortgage |

Investors must cover the margin |

|

Leverage Strategy Options |

BRRRR, house hacking, HELOCs |

Margin trading |

Income-Oriented Investments

Both real estate and stocks can appreciate over time, and both can generate passive income.

But here’s the thing: most stocks don’t generate much income through dividend yield. 2018, for example, the S&P 500 paid a dividend yield of around 1.9%.

Rental properties excel at generating passive income. Most rental investors aim for at least 7-8% in cash-on-cash returns from rental cash flow and consider property appreciation a nice bonus.

This segues nicely into the next advantage: predictable rental cash flow.

Predictability of Returns

No, real estate investors can’t predict housing market movements, just like stock investors can’t predict stock market movements.

But they don’t have to. In the battle of real estate vs. stocks, one enormous advantage is that landlords can calculate a rental property’s cash flow before buying it.

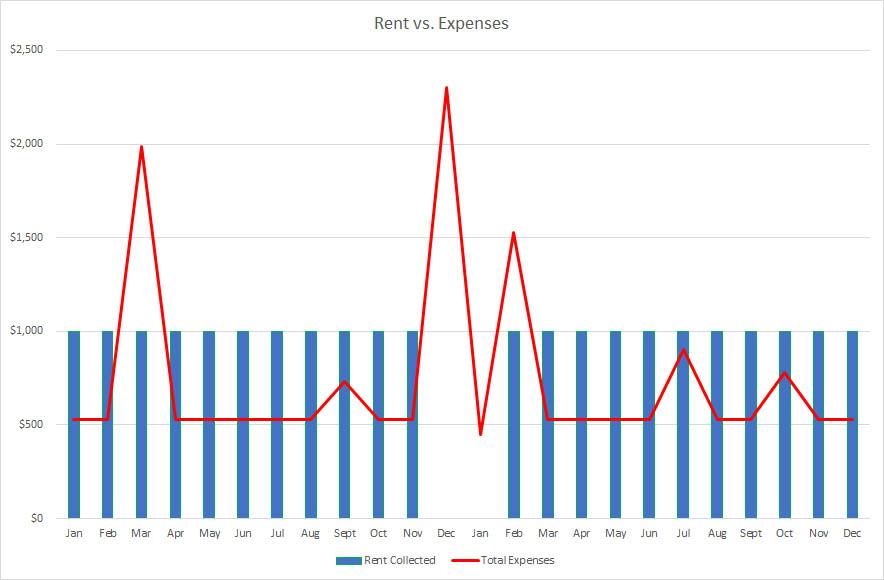

Not on a month-by-month basis, of course. This month, you might suddenly have a $500 plumbing repair, while the next two months will have no expenses, followed by a $1,000 furnace repair bill. Rental income and expenses might look something like this:

However, rental property expenses are predictable in the long term. Landlords can (and should) set aside monthly money for these long-term expenses, such as repairs and vacancies. The rest they can pocket as cash flow.

Use our free rental property calculator to run the numbers on any rental property; here’s a quick overview of how it works:

Rental properties aside, flippers can predict their returns as well. They know the purchase price, they know the cost of repairs, and they know the after-repair value (ARV). While those numbers aren’t always perfect in their precision, the property may sell for $5,000 more or less than expected. For example, experienced investors can pinpoint these numbers accurately enough to earn reliable returns.

Control over Returns

Another win for real estate investing vs. stocks is that real estate investors have control over their returns. They can reduce tenant turnover through better property management. They can upgrade the rental property to attract higher rents and quality tenants.

Landlords can also get creative and add extra revenue streams, which are more ways to make extra money on rental properties.

This control does not end with traditional landlords. Vacation rental landlords can use all sorts of strategies to drive more Airbnb bookings, which will result in a higher occupancy rate and higher returns.

Likewise, flippers can invest more or less in repairs, depending on the difference in ARV.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

Inflation Adjusted Returns

One huge advantage for rental properties vs. stocks is that rents rise alongside inflation. In fact, rising rents are a primary driver of inflation.

Landowners’ mortgage payments stay the same over the years, but their rents rise. Imagine a landlord bought a property in 2010 that rented for $1,000, with a $500 mortgage payment. Ten years later, in 2020, their mortgage payment remained $500, but the rent rose to $1,500. The spread between their mortgage payment and their rent doubled!

That makes real estate an outstanding hedge against inflation.

Alternatively, consider a stock investor. Say they earn a 2.5% dividend yield and see 5.5% from price growth for an 8% return this year. But if there’s 2% inflation this year, their real return is 6%, not 8%.

Landlords don’t need to adjust their returns for inflation, but investors in just about everything else (including stocks) do.

Tax Advantages

Rental properties come with an enormous assortment of tax deductions, including many “paper” expenses that don’t actually cost real money.

For example, you can deduct for depreciation (see our property depreciation calculator), and with the Tax Cuts and Jobs Act of 2017, most landlords can take an extra 20% pass-through deduction.

Best of all, you can take advantage of rental property tax deductions even if you take the standard deduction. Rental property tax deductions are “above the line” and come off your total rental income before it’s added to your adjusted gross income.

Every conceivable expense associated with rental properties is deductible, including travel, home office, and other deductions only available to the self-employed. This abundance of deductions often leaves landlords with a lower tax bill even though they saw profitable rental income.

Greater Stability

Stocks are notoriously volatile. And while home prices can fluctuate, they don’t fluctuate with anything like the peaks and valleys that stocks see.

Since 1963, housing prices have only declined by more than 10% once, during the 2008 housing crisis and subsequent Great Recession. See the median home sale price in the US tracked below, courtesy of the Federal Reserve:

Yet dozens of stock market drops of over 10% (see the chart further down).

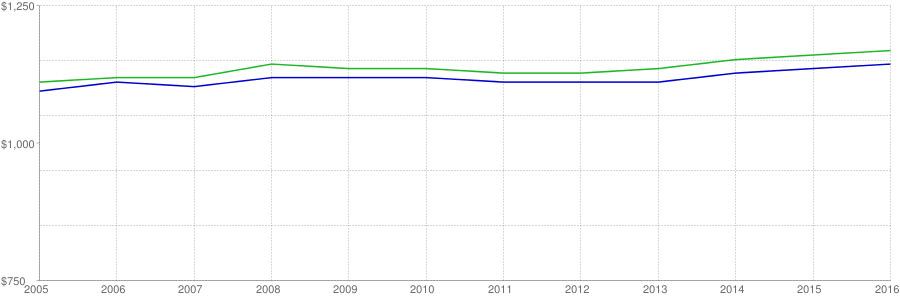

Rents are particularly stable. They rarely decline; when they do, it’s by very small margins. Check out this graph, showcasing how little rents dipped even at the height of the Great Recession (green is average rent, blue is median rent):

That’s one reason why real estate investors can accurately calculate rental cash flow: rents tend to be stable and to only move upward.

Physicality

Real estate is, well, real. You can walk up and touch it. You can physically improve it. It can’t be stolen, it can’t declare bankruptcy, it can’t go out of business.

Yes, real estate can decrease in value. In the Great Recession, the average American home lost 23% of its value, according to Zillow. But stocks can literally lose 100% of their value overnight—they’re paper assets based on legal entities. There’s nothing inherent in their value.

Your rental property isn’t going anywhere. If it burns down, you have insurance. It has inherent value, which is why banks will lend 96.5% of its value to you and why they only lend 50% of the value of stocks on margin.

Disadvantages of Real Estate

I love real estate as an investment, but it’s not all rainbows and butterflies, believe me.

Here are some of the disadvantages of real estate vs. stocks, even when reaching financial independence and retiring early.

Lack of Liquidity

Real estate takes time to buy and sell. It’s taken me upward of nine months to sell a property!

That means if you encounter a financial emergency and need money now, real estate won’t bail you out. It will take at least a month or two (often longer) to sell and a similar time frame to borrow against.

High Barriers to Entry

One reason for the impressive returns and perks of real estate investing vs. stocks is that it’s harder to invest in real estate. The barriers to entry are higher, which cuts both ways. It makes for great opportunities for investors with plenty of money and experience, but it also makes it difficult for newbies to enter the fray.

A 20% down payment, plus closing costs, plus cash reserves? That’s tens of thousands of dollars. At least. And the average American doesn’t have $30,000 sitting idly by and collecting dust.

Nor is cash the only barrier to entry. It takes knowledge and skill to find good deals on rental properties. It also takes knowledge and skill to manage properties effectively (although you can delegate that work to a property manager if you like).

There’s even an element of knowledge in creating a down payment. Try these ideas for how to come up with a down payment on a rental property.

Labor

Buying real estate takes work, as does overseeing renovations for a flip, managing rental properties, and preparing a property to sell.

It’s a key difference between real estate investing vs. stocks. You can buy a stock, ETF, or mutual fund in 30 seconds and promptly forget about it. There’s just no comparison with real estate investing.

With that said, there are plenty of tools to reduce the work of real estate investing. For example, you can analyze and buy turnkey rental properties on Roofstock. Read our full Roofstock review here, and below is a quick overview of how it works:

Or you can instantly find local vacant properties, foreclosures, divorces, judgments, and other distressed sellers using Propstream. Likewise, here’s our full Propstream review.

If you’re driving for dollars to find deals, try DealMachine. They’ll instantly pull up the owner’s name, contact information, and mortgage amount, and with a click of a button, you can have DealMachine send a written mailer to the owner.

And, of course, we provide automated landlord software. It helps you automate rent collection, advertise vacant units on many websites, screen tenants, build state-specific lease agreements with just a few clicks, and even outsource your maintenance and property repairs. Still, online landlord software and services can help you automate real estate investing work – but not remove it entirely.

Diversification Difficulties

Each property costs so much of your capital, making it harder to diversify.

Imagine you have $120,000 to invest. You could buy one $120,000 property in cash or finance four rental properties requiring $30,000 apiece in down payments and closing costs.

Or you could buy shares in thousands of companies across dozens of countries.

That said, nowadays, you can easily diversify with real estate crowdfunding investments. For example, with $10, you can invest in dozens of properties through Fundrise. Or you can buy shares in commercial office buildings through Streitwise, earning 8-9% dividends plus appreciation.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

Advantages of Stocks vs. Real Estate

So, what are the pros of investing in stocks vs. real estate?

Yes, I’m a “real estate guy,” but that doesn’t mean I don’t love stocks. Stocks have some undeniable advantages, and no retirement portfolio is complete without a diverse set of equity holdings.

As you explore stocks vs. real estate for FIRE, try playing around with this FIRE calculator from How to FIRE. Working with real numbers makes financial independence and retiring early tangible rather than a pleasant daydream.

Liquidity

You can buy and sell stocks instantaneously.

Got hit with a $5,000 medical bill and need money right now? Sell some stocks, and you have cash in hand today.

Of course, that same ease of buying and selling drives stocks’ notorious volatility. Stock markets can fluctuate wildly based on a single financial news story. It may be forgotten entirely by tomorrow, and the market swings in the other direction.

But there’s a certain reassurance in knowing that if you want your money out today, you can have it out today.

Low Barrier to Entry

Have an extra $100 sitting in your bank account? You can invest it in stocks with few headaches, knowledge, or costs.

No, really. You can open a brokerage account (I personally use Charles Schwab, but Vanguard is excellent as well), transfer money into it, and buy a low-cost index fund that tracks the S&P 500, Russell 2000, or some other stock index. Accounts are free to open, and Schwab recently stopped charging commissions when you buy and sell.

In other words, stock investing is completely free. If you buy an index fund, even the fund management fee is extremely low.

Don’t get me wrong, evaluating and picking individual stocks takes knowledge. But you don’t have to go that route – you can simply invest money “in the market” by investing in an index fund. No skill is required.

There’s no equivalent option when buying a rental property or flipping a house.

Easy Tax-Free Retirement Contributions

You can invest in stocks tax-free for retirement with an IRA, 401(k), or other related retirement accounts.

And it’s easy – within five minutes, you can set up an IRA through your brokerage. Buying or selling stocks in your IRA account is no different than in your brokerage account.

That said, you can also invest in real estate through a self-directed IRA. But it’s a little more complicated, and you must go through a trust company to administrate it.

Easy Diversification

With $100 and a few clicks, you can invest in index funds that own hundreds of companies. You can invest in US stock funds, European stock funds, Asian stock funds, and emerging market stock funds.

Small or large market cap in sectors ranging from technology to healthcare, energy, and beyond. It’s incredibly easy to diversify your stock portfolio.

Why does diversification matter? In a word, risk. The idea is simple, and an old proverb sums it up nicely: don’t put all your eggs in one basket.

Diversification is one of the great advantages of stocks vs. real estate.

Completely Passive Income

When you buy shares in an index fund, you can let them sit there, compounding as dividends reinvest, until you’re ready to retire. The only second thought you might have is rebalancing, and even that can be done passively through “cash flow rebalancing” (adjusting new stock purchases to shift your asset allocation as desired).

In the debate over real estate vs. stocks, sometimes proponents of real estate gloss over the fact that rental properties are not a passive income source. It takes some labor to manage rental properties. Even if you outsource that labor to a property manager, you’ll still occasionally get phone calls from them asking for a check for $2,500 to replace the furnace.

Your stocks won’t call you at 4 AM complaining that a light bulb blew out, but your tenants might.

Disadvantages to Stocks

I touched on some of these above already when reviewing some of the advantages of real estate investing vs. stocks. Keep these disadvantages in mind when deciding between real estate and stocks.

Volatility

Stocks swing wildly in value. Real estate doesn’t.

That matters because volatility represents risk. If you buy a stock, high volatility means higher unpredictability. It could drop by 50% or rise by 50%; you buy it and hope for the best.

Check out the S&P 500’s gyrations from 1928-2022:

Economists measure risk vs. return of an investment by dividing its average annual return over its volatility (measured by the standard deviation of the return). This is called a Sharpe ratio, literally a ratio of return over risk.

Remember that 145-year study I mentioned at the outset? Stocks had a Sharpe ratio of 0.27, while real estate had a Sharpe ratio of 0.7 – a much better ratio of returns over risk.

No Control over Returns

When you buy a stock, your only control is when to sell it. You have zero control over its performance.

The company’s earnings could drop. Its CEO could be fired for a sex scandal. Or a competitor could buy it out, and shares could skyrocket. None of which you can control.

No Predictability of Returns

Likewise, stock investors can’t predict any of those swings in value. You don’t know if earnings will rise or fall or a merger will occur. You just buy and hope for the best.

A huge advantage of real estate vs. stocks is that investors can predict returns.

Sequence Risk

Sequence risk is a lengthy conversation, but here’s the short version. When you first retire, a stock market crash would have a much greater impact on your returns than if it happened later in your retirement.

It’s a little counterintuitive, but the order – the sequence – of your returns actually matters just as much as the long-term average. A crash right after you retire can put such a large dent in your stock portfolio that it’s hard to recover.

But if a stock market crash occurs later in retirement, after years of strong returns, your portfolio may have reached a “critical mass” where it can survive a bear market with less trauma.

Here’s exactly how rental properties can reduce sequence risk and a reminder of how real estate complements stocks in your retirement portfolio.

The Data on Real Estate vs. Stocks for FIRE

First of all, what do stocks earn on average?

The S&P 500 (an index of large-cap US stocks) has returned an average of roughly 10% annually since its inception in 1928. About 40% of that long-term average has come from dividends – in a perfectly average year, the S&P 500 might return a dividend yield of around 4% and see a 6% increase in stock prices.

With that said, inflation has averaged around 3% over the last 90 years, which must be subtracted to determine the real return. In adjusting for inflation, investors could expect a return of around 7%.

Of course, stocks don’t just rise slowly and steadily. They leap by 25% one year, collapse by 20% the next year, and wobble the next. See the S&P 500 chart above.

Meanwhile, home prices average around 5.3% annual appreciation. However, that doesn’t include inflation and doesn’t account for US homes growing larger during that period.

Besides, we’re not concerned with appreciation if we’re interested in FIRE. It won’t pay our bills, but rental cash flow will, and rents will adjust for inflation (more on that below).

Sample Numbers for FIRE: Stocks

Stanley invests only in stocks, while Rachel invests only in rental properties. We’ll be generous and give both of them 10% returns. Both want $50,000/year in income from their investments to cover their living expenses in retirement.

Stanley plans on selling 3.5% of his stock portfolio every year to live on upon reaching FIRE. That number is not arbitrary – financial planner Michael Kitces has demonstrated that investors can withdraw 3.5% yearly and never run out of money. Compare that to the traditional “4% Rule;” investors who sell off 4% of their investment portfolio yearly can only depend on it for around 30 years.

If Stanley wants $50,000/year in income, he needs a nest egg of $1,428,571. Wait, huh? Don’t fret—the math is actually super simple: 3.5% of $1,428,571 = $50,000.

But that’s a lot of money. Stanley needs to save $1,428,571 in ten years, with a 10% return, or $89,636.25 a year.

No small feat. I hope Stanley earns a good income!

Sample Numbers for FIRE: Real Estate

Rachel buys properties for $100,000 apiece, rents them for $1,500, and has around $670 in monthly expenses. That leaves her with $830 monthly in profit/cash flow – a return of around 10%.

Except Rachel doesn’t pay cash for her properties. She finances them with a 30-year rental property loan and puts down 20%, or $20,000. At a 6% interest rate, she pays $479.64/month for principal and interest. That lifts her total expenses per property to around $1,150 for a monthly cash flow of $350.

But it also lifts her cash-on-cash return. She invests $20,000 in cash and gets back $4,200/year, boosting her cash-on-cash return from around 10% to over 20%.

It would take 12 properties earning $4,200/year to generate $50,000 in income. At $20,000 a pop, that comes to $240,000 in down payments—a far cry from the $1,428,571 that Stanley needs!

This is why I love to argue that rental properties bend the normal retirement planning rules!

Correcting for Oversimplification

The numbers above are oversimplified, of course. They don’t include closing costs, and critics would object that it’s hard to find real estate deals with returns that high.

But that simplicity cuts in the other direction, too. We didn’t add money for Rachel’s property appreciation. We didn’t deduct money for Stanley’s brokerage fees or account for the inflation that Stanley will face.

Rachel’s rental income, meanwhile, will automatically rise to adjust for inflation and, in all likelihood, rise faster than inflation.

Alternative Investment Models

Most people think investing in real estate requires massive down payments, and stocks are your only option. But think again. Modern investment platforms have created some interesting alternatives for FIRE seekers.

Real Estate Crowdfunding

As mentioned, platforms like Arrived and Groundfloor have entirely changed the barrier to entry. Instead of scraping together $30,000 for a rental property down payment, you can start investing in real estate with as little as $10. These platforms let you:

-

- Own pieces of multiple properties

- Earn quarterly dividends

- Benefit from property appreciation

- Avoid tenant headaches

- Diversify across different markets

Check out our charts comparing real estate crowdfunding platforms.

Other Passive Real Estate Investments

Don’t you want to tie up your money through crowdfunding? No problem. Real Estate Investment Trusts (REITs) trade just like stocks but invest purely in real estate. They’re required to pay out 90% of their profits as dividends, often yielding 4-8% annually.

The downside: REITs share a strong correlation with the stock market.

For true diversification consider real estate syndications, private partnerships, private notes, and other private equity real estate investments. In fact, we go in on these hands-off real estate investments every month in our Co-Investing Club with small amounts.

Our goal: to find investments offering “asymmetric returns,” or high return potential with low downside risk.

Perhaps the best part is that you can mix and match these alternatives with traditional real estate and stock investments. You see, it’s not about choosing just one path to FIRE – it’s about finding the right combination that works for your goals and risk tolerance.

Real Estate or Stocks for FIRE? Invest in Both

Yes, in the sample numbers above, reaching FIRE with real estate is far faster than with stocks. But reaching FIRE isn’t just about dollars and cents.

Financial independence and early retirement also depend on security and risk management. As you know by now, diversification is crucial for risk management.

I personally recommend investing in rental properties for income and stocks for growth and diversity. Why choose only real estate or stocks? Invest in both, and get the best of both worlds.

If you encounter a true financial emergency, you can liquidate stocks for immediate cash. If your stocks have a terrible year, you can lean more heavily on your rental properties and not sell any stocks.

Your savings rate is less important than whether you invest in real estate vs. stocks. If you can live on half your income or even less, you can reach financial independence quickly.

The trick to reaching FIRE is trimming expenses and pumping every penny into investments. Real estate investments, stock investments, private notes, bonds; just start building an investment portfolio. Check out our free FIRE calculator to play around with different numbers.

You’ll learn as you go, but there’s no getting back lost time!

What’s your plan for reaching financial independence and early retirement?

Connect with us on social!

Great breakdown of the pros and cons of real estate investing vs. stocks. I too invest in both, and look for income from my rentals (plus tax deductions) and growth and tax-free returns from my Roth IRA.

Way more comprehensive breakdown than I’ve seen elsewhere, thanks for a good one Brian!

Glad you found it useful Chelsea, thanks for the comment!

I do not have much experience with stocks but I would love to learn. I currently have been working on my real estate portfolio and would love to reach early retirement through them.

One of our core tenets is “Passive income through real estate, growth & diversification through stocks.” Investing in stocks is way easier than investing in real estate – just start with a handful of index funds. Or just use a robo-advisor to make it even easier!

Real estate is the safest way to invest your hard-earned money. At least if you know what you’re doing (many new investors dive in without mastering the fundamentals).

If you are looking for a long term investment for passive income, you should definitely go for real estate.

I hear you Humayoun! And I’m glad to hear you’ve had success with your long-term real estate investments!

I always view rental property business as a supreme business that offers various benefits and has a power to make people wealthy. For the stock market, I think the first time Investors should stay away from investing in stocks if they don’t have a prior experience. Similiar with REITs. The entry barrier sure is high with real estate but investing in stocks over it is not an alternate.

I personally invest in rental properties for immediate, ongoing income protected against inflation, and tax advantages outside of tax-sheltered accounts. I invest for stock index funds for diversification, long-term growth, and ease of investing in tax-sheltered accounts.

So for me, they serve different goals. But you don’t need to be an expert in stock investing to do it, you can simply use a passive investing strategy like I do, in diversified index funds through a robo-advisor (I use Schwab, which is free).

Brian, you said it right. Stocks for diversification is always a good idea. But, in my view, people must first acquire real assets aka real estate and then think of investing in the stocks with money made from real estate in order to diversify the portfolio. What u suggest?

Hey Mannu, the earlier you can invest in stocks the better, since the returns compound over time, and completely passively. One nice thing about stocks is you can invest with a few dollars if that’s all you have, whereas direct real estate investing requires thousands in down payments. But to me, they serve different purposes, so I want both simultaneously.

Acquiring Rental Properties is one of the safest way to create wealth. Why invest in something which is not in your control aka the stocks. Moreover, if you are someone who has limited money to invest, why the heck you want to take risk with stocks? Stocks have high volatility and for a beginner investor, there is real hard to differentiate between a speculation and the right stock. Better safe than sorry.

Real estate might have a little higher entry point but it can be managed if you know how to use the leverage the right way.

Though I’ve not proper knowledge about stock, I really have an interest in this. I learned something from that article. As my background relies on civil engineering, I want to do something in the real state sector.

Glad to hear it was useful for you Maria!

We are vibing! I also wanted to invest both Real Estate & Stock. Glad to read this article!

Haha, glad to hear it Ivan!

When you are young and want instant money, then it is possible for you and you have the strength to invest in stocks and the securities market! But over time, you want need most is stability! That’s what the real estate market is for!

Haha, well, real estate is definitely more stable than stocks 🙂

Hi Brian, I stumbled on your website today after complaining to a friend that most FIRE content does not take rental properties into account when calculating your FI target. Glad to find someone who has thought this through! My spouse and I bought our first multifamily in 2012 with an FHA (refinanced to a conventional a year later) before the term “house hacking” was really bandied about; in fact, we learned that from his parents who were effectively house hacking back in the 80s!

Since then we have invested in additional real estate for rental income, including a condo in our college town area, which we rent out to students. More recently, we moved out of our part of the multifamily and bought a fixer-upper in a better, more walkable neighborhood, which we renovated (and then refinanced at the appreciated value). Most people around us assumed we would sell our previous home to pay for the new one. Our response: why on earth would we sell a positive cashflow property?

Our experience with rising rents on flat mortgages worked out quite like your examples (not the same $$s but similar principles). The inflation benefits have been crystal clear during these last few years, with rents in our area soaring. Once our (15-yr) mortgages are fully paid off, some of which are inching closer, our expenses will go down even further and the monthly rental income will significantly increase.

Bottom line, our rental income is bound to be our biggest contributor to FI by a mile, over and above any stock portfolio contributions. I say this as someone who has been investing in stocks since I was 19, who maxed out my Roth IRAs while being the proverbial “starving grad student”, and whose retirement advisor after reviewing our retirement accounts in a recent meeting suggested that my spouse and I “take the kids to Disneyland, because you can’t take all that money with you” (no joke). Nonetheless, as important a role as my stock portfolio plays in my FI journey, that monthly income generator in the form of rental properties is most likely going to be the key that makes early retirement feasible for us, sooner rather than later, and with a comfortable margin.

So glad to hear you’ve had success with your rental income Shiri! Out of curiosity, what are your plans for financial independence/retiring early?

This article is loaded with prejudice against stock investing, which I suppose is to be expected from a website called SparkRental.

These problems are not addressed:

1. Real estate provides almost no diversification for an individual. You are hostage to one market in one geographic location. The chart of averages shows a happy upward line, but an individual can’t count on getting an average. The fortunes of real estate in one city can vary wildly depending on local conditions. For example, the loss of a major employer can depress prices for years. I’ve lived through such a situation. We bought our house in a housing recession in 1988. It was great for buying, but we had little value appreciation for many years, way below the inflation rate or the return from safe bonds.

2. Landlords have second jobs. If I took a regular second job, my entry cost is zero and my ROI is infinite. If both jobs pay well, I’m well on my way to FI. And presubably my second job mostly uses existing skills, so I probably don’t have to become an expert in a totally foreign subject.Sure,you can outsource the hardest landlord work — for something like 10% of your gross. Only hedge funds charge more for doing the hard work in the financial field.

3. You basically say only securities analysts should buy individual stocks. You’re conveniently assuming a level of expertise in real estate comparable to the expertise of a securities analyst.

4. Let’s say I’m not a securities analyst and am foolhardy enough to buy individual stocks. If I load up on startup biotechs, I could lose all my money. But an amateur won’t go broke with a sensible lineup of stocks like Microsoft, utilities, Ford, etc. Compare that to the experience of an amateur buying real estate. They won’t lose all their money, but if they mess up their first investment, theyre in big trouble. A prudent stock investor can start small and make a lot of mistakes without causing a catastrophe.

Love the pushback William! And you’re right when you talk about landlords having second jobs, and about the challenges of diversification when you invest $50-100K in a single real estate investment. That’s precisely why we do what we do in our Co-Investing Club: members get together and vet group investments, and invest $5K per deal passively, with no active role in managing assets or properties. That makes it easier to spread relatively small amounts across many markets and property types.

I appreciate your open-mindedness.

And I strongly agree that a cooperative approach is best for those who don’t have a highly advanced level of expertise in the field.

Absolutely William!