The Big Picture on Questions To Ask Before Buying Rental Property:

-

- Unlike stocks or REITs, selling real estate is time-consuming and costly, often taking several months and thousands of dollars.

- Successful rental property investors need to identify their competitive edge—whether through cash purchases, fast deal closures, renovation skills, or off-market property access.

- Deciding who will manage the property—whether self-management or hiring a property manager—directly impacts profitability.

Disclaimer

The information provided on this website is for general informational purposes only and should not be construed as legal, financial, or investment advice.

Always consult a licensed real estate consultant and/or financial advisor about your investment decisions.

Real estate investing involves risks; past performance does not indicate future results. We make no representations or warranties about the accuracy or reliability of the information provided.

Our articles may have affiliate links. If you click on an affiliate link, the affiliate may compensate our website at no cost to you. You can view our Privacy Policy here for more information.

Unlike flipping, buying a rental property is a long-term investment, and long-term investments require long-term thinking and planning.

Real estate is an inherently illiquid investment—unlike stocks, bonds, or REITs, it costs several months and thousands of dollars to sell. Selling a rental property could take six months and $15,000, a far cry from selling stocks instantly at a $4.95 commission to a broker.

That means that making a mistake when buying a rental property is not solved as quickly, easily, or cheaply as selling a stock you decided you don’t like.

So? Don’t make mistakes!

Top Questions to Ask When Buying A Rental Or Investment Property

Yeah, that’s easier said than done. But the great thing is that you’re not the first person to invest in real estate, so there are tons of sources where you can ask questions about buying your first investment property!

If you do it right, your learning curve will involve minor missteps rather than regret-induced migraines.

Here are nine questions to help you make rational, well-informed rental investing decisions and ensure your next rental property is a winner.

1. When were the roof, furnace, AC unit, and water heater last replaced?

Of course, there are other components to any house that you need to evaluate. However, these three things can be a good way to determine if a rental property is a good investment.

Some components, such as the framing, wiring, and plumbing, have extremely long lifespans, and the cosmetic updates are obvious enough. You don’t need me to remind you to look at the kitchen and bathroom; you know how dated or chic they are.

But it’s not necessarily obvious how old the roof, furnace, air conditioning unit, and water heater are. These can be expensive to replace, and if they need to be replaced within the next few years, you should know it before buying the rental property.

First, ask the seller. If they can’t give you a precise answer—preferably with documentation—get expert opinions. Ask your Realtor, contractors, and home inspector.

This brings me to my second point: always get a home inspection. Even if you’re buying the property as-is, you need to know what you’re getting into.

Here’s a quick reference infographic showing how long each component in a property lasts so you can get a sense of how frequently you’ll need to replace them.

2. What is my competitive advantage as a real estate investor?

Now, here’s one of the most critical personal questions to ask before buying rental investment property—or getting into any endeavor, for that matter.

When you’re in business, you need a competitive advantage or three. And make no mistake: as a real estate investor, even a solo investor buying your first rental property, you’re in business.

You don’t have experience, so don’t count on that as your advantage. What about cash? Can you buy rental properties in cash rather than taking out a rental property loan?

How quickly can you settle if you’re using a rental property loan to buy the property? Speed can be a competitive advantage.

Perhaps you can find good deals on rental properties that other investors are missing. One way to do this is by finding properties not listed for sale and approaching the owner directly about selling. Try Propstream or DealMachine, which are powerful real estate tools to help you do this.

If you’re not familiar with it, here’s our full Propstream review, plus a two-minute overview of features:

Another competitive advantage can be your networks of off-market sellers, such as wholesalers and turnkey sellers. We include a directory of them, the Dealfinder Database, along with our FIRE from Real Estate course, but there are plenty of other ways to renovate the network as well.

Your competitive advantage could be that you can do the renovation work yourself or that you can make offers so quickly that you get properties under contract within a few hours of them being listed. Whatever your competitive advantage, make sure you’re clear about it!

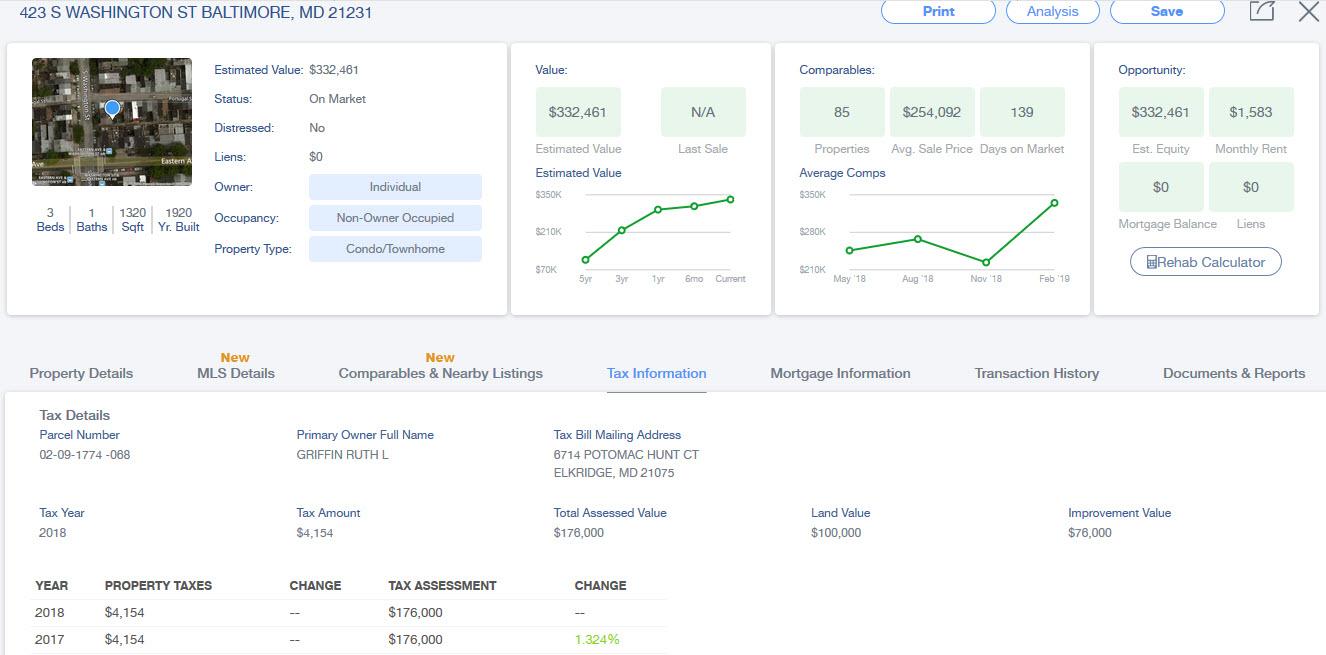

3. What’s the property tax bill, and will it change when I buy the rental property?

The last thing you want is a nasty surprise when you discover that the tax bill suddenly doubled from $2,000/year to $4,000/year upon the property’s sale.

Many jurisdictions update their tax assessment value of the property when it transfers. If the property is currently assessed at $100,000, and you buy it for $200,000, that can cause the tax assessment to jump to (you guessed it) $200,000. Read double taxes.

So, you need to check on the current tax bill and assessment. One way to gather this intelligence is through Propstream, which displays it for you:

Calculate the potential property tax bill based on your purchase price if the tax assessment value is significantly lower than your price to buy the rental property. A quick Google search will reveal property tax rates in the property’s jurisdiction.

Use that new, higher property tax bill when you calculate the rental property’s cash flow.

(article continues below)

Free Masterclass: Financial Independence in 5 Years with Rental Properties

4. What’s the neighborhood vacancy rate?

How and what to forecast is one of the best questions to ask before buying any rental property. Just as you need an accurate number for the property’s tax bill, you also need an accurate estimate of its vacancy rate.

The vacancy rate is an expense that many new rental investors ignore. But over time, vacancies will eat into your average cash flow, making it a real expense.

Talk to other neighborhood landlords and property managers to understand the local vacancy rate. For online resources, Moving.com (shown below) provides some insights into local vacant properties, and Propstream displays vacant properties based on your search parameters.

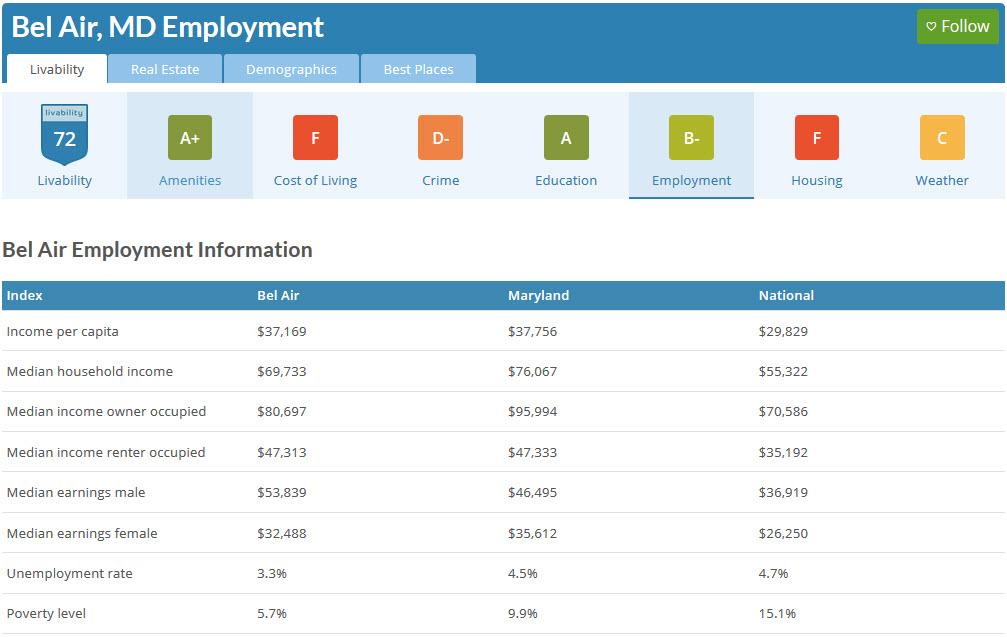

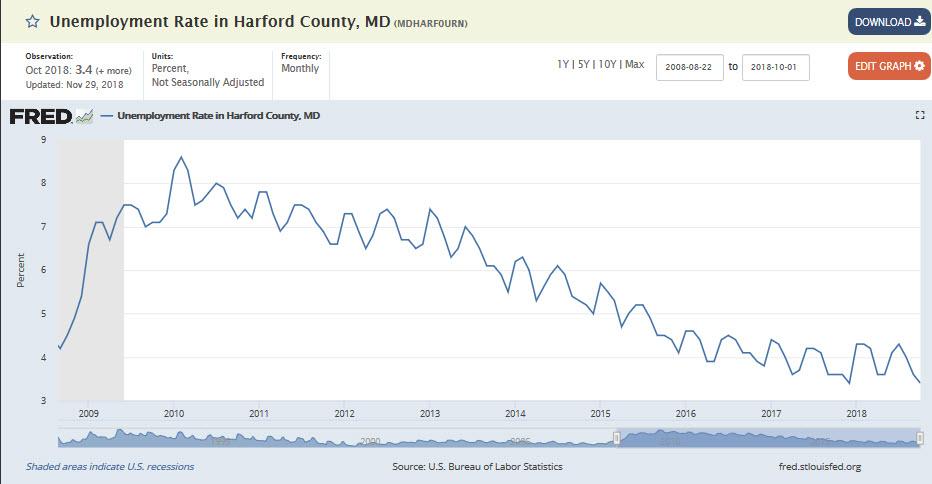

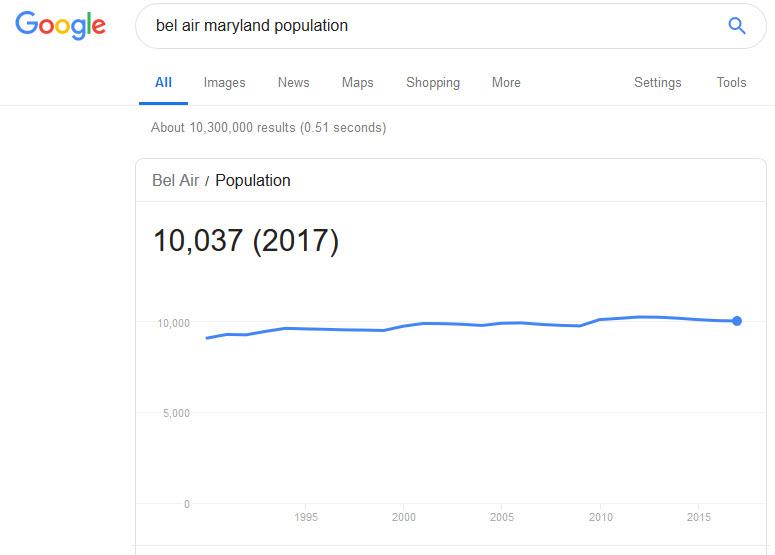

5. What direction are economic and social indicators trending?

Never buy a rental property without understanding the local economic trends.

Most notably, these include crime rates, unemployment rates, population, and income. Check crime rates and unemployment rates on the local level using AreaVibes:

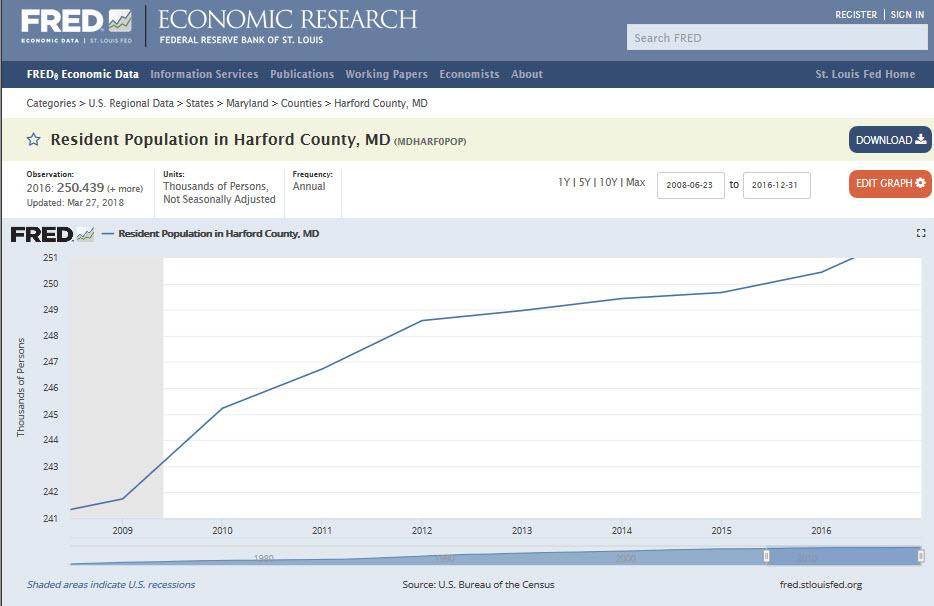

For county-level data, check the Federal Reserve:

You can find town-level population growth on Google:

And county-level population growth on the Federal Reserve:

Rising population and income are promising signs, as are shrinking unemployment and crime rates (thank you Captain Obvious). Ensure you have your pulse on the local economy, which goes beyond looking up data online.

Go walk the neighborhood and talk to local business owners. Get a true gut-level feel for what’s happening in the area, and only invest in neighborhoods and towns on the rise.

6. Who’s going to manage the property?

This is an important question before you get into rental properties, and there’s no wrong answer here. But you do need an answer and a good reason for it.

If you manage the property yourself, you can avoid paying a property manager – but managing a rental property is still a labor expense, even if you do the labor yourself. When calculating the rental property’s cash flow, include property management as an expense either way.

Managing your first few rental properties can be an excellent education, and I highly recommend it. It makes you a better rental investor because it forces you to develop a better sense of what tenants look for, how to buy rental properties that will attract good tenants, and the job of being a landlord.

You can always outsource property management later after you’ve gotten the hang of being a landlord.

To make your life easier as a solo landlord, we offer free landlord software that helps you automate your property management. Here’s a quick overview of exactly what you can do with our landlord app:

Before buying a rental property, you need to answer the questions, “Do I want to get involved in the every-day management?” and “Who will run the show?”

Once you buy a rental property, someone needs to be on the front lines managing it, and you don’t want any confusion about who that is.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

7. How does my cash-on-cash return compare to other potential investments?

Now, here’s a question you need to ask when getting into any investment: rental properties, stocks, REITs, fractional real estate, etc.

You have a limited amount of money. You want to invest it where it will reproduce faster for you.

Buying a rental property can deliver excellent returns, especially in the form of passive income. But every property and market is different, and you need to be able to quickly compare returns not just between rental properties but against other types of investments.

Say you run the numbers on a property on a rental property calculator and determine it will pay an 8% cash-on-cash return in rental income, not including appreciation. (For reference: “cash-on-cash return” means the return not on the property’s total purchase price but on your own cash investment if you’re financing it with a rental property loan.)

So, you can earn 8% a year on rental income from Property A, plus any appreciation. What about an alternative Property B? Or buying stocks? Or a REIT, investing in a crowdfunding website, or something else entirely?

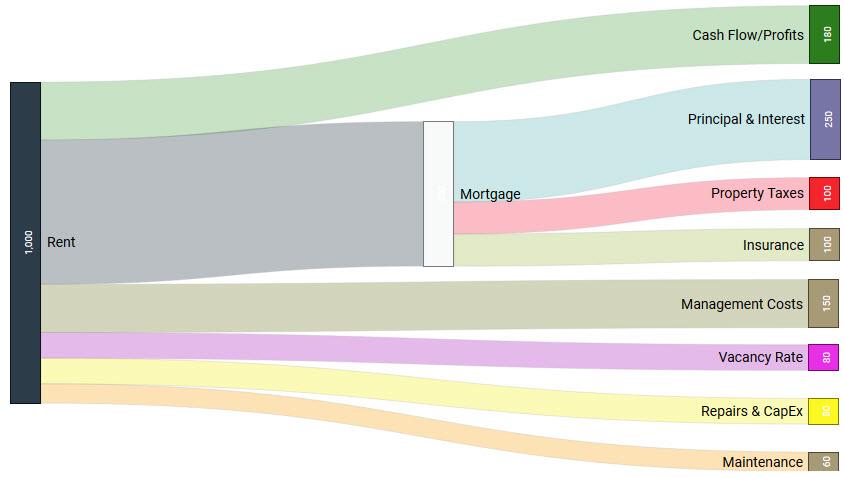

One of the great advantages of buying rental properties is that you can accurately calculate their returns. It’s not their appreciation but their rental income returns because they’re based on today’s numbers. You don’t have to wonder how fast home values, rents, or stock values will go up; you know your expenses and the market rent.

I’ll leave you with this Sankey diagram to help you visualize how real estate cash flow looks:

8. How transitory is the neighborhood?

Turnovers are where most of the work and expenses lie for landlords. To earn more and work less, you want to minimize your rental property turnovers.

Unlike many questions above, this one can’t be answered with an app or a handy real estate investing tool. You must talk to other local landlords, property managers, and Realtors. Talk to local business owners and residents. This question is crucial to ask when considering buying a house with tenants.

Do people set down roots and raise children in this neighborhood? Or do they hang out for a few years in their early-mid 20s before moving out to the suburbs when they get sick of the crime and high taxes? (Sadly, that was the case in the downtown neighborhood where I lived for much of my 20s and early 30s.)

High turnover rates will kill your profits, as a long-term rental landlord. But they won’t hurt you if you rent the property short-term on Airbnb.

9. How do the cash flow numbers compare to a short-term rental?

Some properties earn more as long-term rentals. Others earn more as short-term rentals, even accounting for greater management expenses and labor.

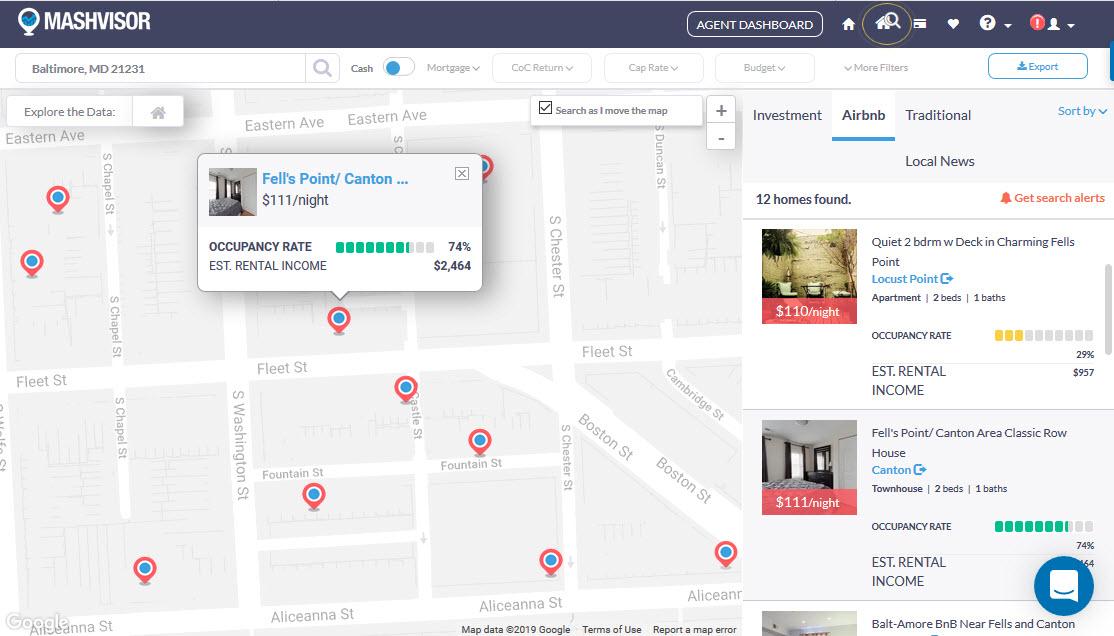

Check out Mashvisor as a tool to help you compare long-term and short-term rental property returns. Mashvisor analyzes occupancy rates as a factor when they run the local numbers for you since occupancy rates have such an impact on landlord returns.

Here’s how it looks:

You can click on individual properties for more details or to view the full listing on Airbnb.

While you’re making up your mind, check out these Airbnb success tips for new Airbnb landlords, or you can check out this masterclass we held with Airbnb expert Al Williamson.

Final Word On Questions To Ask Before Buying Rental Property

Buying a rental property is nothing like buying a stock, so it’s only fair to ask questions beforehand. It takes time, it takes effort, it takes a lot more money to come up with a down payment, and you can’t sell it on a whim.

But for all that, rental properties come with some unique advantages. You can accurately forecast your cash flow and returns before buying a rental property. You have a degree of control over those returns in your approach to property management. Rental properties are far less volatile than stocks in terms of property values and rents.

And speaking of rents, they rarely decrease.

Before you buy your first rental property, make sure you know what you’re getting yourself into. We offer plenty of free education, from our rental income blog to our webinars to our free rental investing course, but we’re not the only source of education out there. Read everything you can, join webinars, and listen to podcasts because the more you know before buying a rental property, the more likely you will earn good money.

More for New Real Estate Investors:

I want to know more about…

Connect with us on social!

Great roundup of questions new real estate investors should ask before sinking hundreds of thousands of dollars into a property!

Wish I’d read something like this before I started investing, would have saved me a lot of money…

Thanks Eddie! And better late than never 🙂

Awesome….great contents, very very informative.

I am new like a new born baby, have no knowledge of REI.Ih

I have a question, if i see a sale by owner sign, how do you approach to owner, how to start conversation or how to talk to them what ask ,what to say, etc is there is script or something…pl. advise.

Thanks Sam! I’d simply call and ask simple follow-up questions about the property’s condition and the seller’s urgency, and if you like what you hear, schedule an appointment to walk through the property. There’s no one-size-fits-all script, just get a sense for whether the deal is worth pursuing before investing the time to walk through in person.

Keep us posted on how we can help!

Great article guys!Thanks for sharing with us 🙂

Much appreciated!

Greate article guys, Thank you for giving me this information.

Glad you found it helpful RPM!