Remember the housing bubble, real estate market crash, and Great Recession in 2008?

I do. It was an utter nightmare for me and millions of other property owners, representing the second-largest recession in American history, junior only to the Great Depression. Given that a real estate bubble largely caused it, many Americans worry we’re experiencing another housing crash in 2023.

I get it. Median U.S. home prices skyrocketed 42.2% in the four years from January 2020 to the same time in 2024. Frothy looking numbers, raising concerns about a housing bubble in 2024. Fears exacerbated as hundreds of cooling real estate markets have already lost value since mid-2022.

Here’s what the data shows about whether a real estate bubble is about to burst — and exactly how housing bubbles work in the first place.

Key Takeaways:

-

- A housing bubble forms when real estate prices rise faster than true demand relative to housing supply.

- Some cities in the U.S. have seen home prices fall over the last 18 months, where prices outpaced demand in the pandemic. Most cities have not seen falling real estate values however.

- While nearly 700,000 new rental units are scheduled to hit the market in 2024, the U.S. will continue to have a housing shortage numbering in the millions of units.

What Is a Housing Bubble?

To better understand if there’s a real estate bubble in 2024, we need to first understand what exactly a housing bubble is.

A housing bubble forms when home prices rise higher than the market’s fundamentals can justify. Fueled by speculation rather than inherent demand for housing, these artificially high property values prove unsustainable over time.

Imagine a neighborhood that appreciates steadily for eight years in a row. Speculators notice, and begin offering a premium for those homes greater than their market value, increasing demand. In turn, homeowners begin selling at inflated prices because of the increased demand. Homebuyers start scrambling to buy into the neighborhood, worrying they’ll get priced out if they wait any longer.

At a certain point, demand dries up because no buyers can afford to pay the inflated prices. The artificially high prices come crashing down, thus causing the bubble to “pop.”

Sure, there are other factors that can contribute to a housing bubble, but this general outline offers an idea of what a housing bubble is.

Housing Bubble Timeline

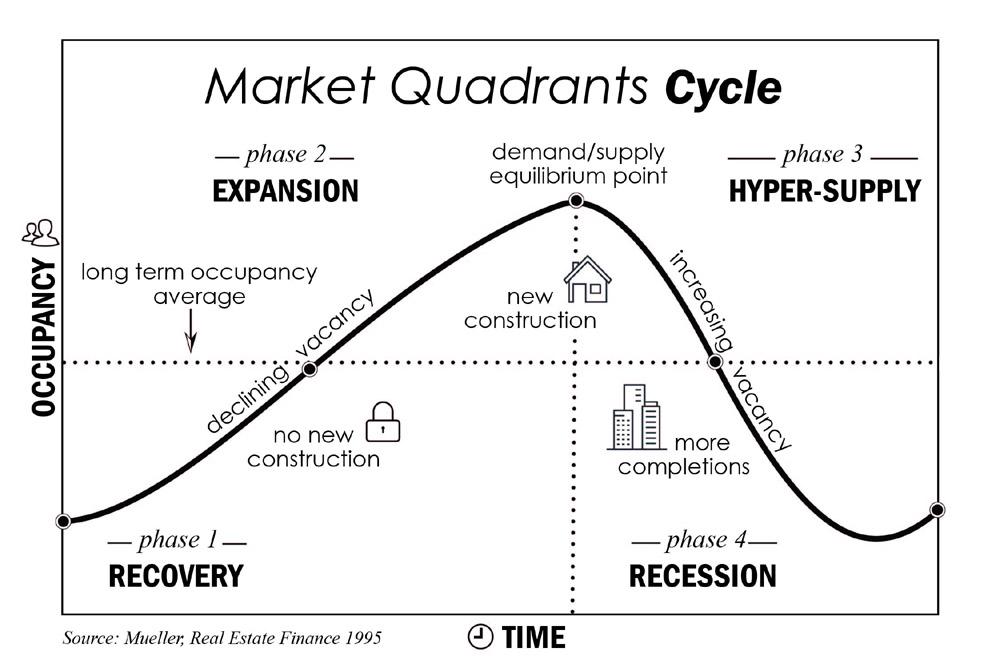

Going a step further, real estate bubbles typically go through four predictable phases.

Phase 1: Properties in Demand

It starts with a market where people actually want to live.

The housing demand is real, and causes prices to rise faster than the surrounding areas. That begins to attract both speculative investors and homebuyers reaching beyond their comfortable price range.

Phase 2: Expectations of Appreciation

In the second phase, excitement and high expectations begins spilling into the decision-making process. Buyers assume that prices will continue appreciating at the current faster-than-average rate.

That assumption of future growth, rather than market fundamentals like local incomes, fuels higher pricing. See the circular logic?

“I’ll pay more for this property because I know future buyers will soon pay even more.”

That sense of buying frenzy spurs developers to build ever more supply as well. But it takes time to build homes and apartment buildings, often measured in years, which means developers fall behind the market fundamentals.

Here’s what the housing market cycle looks like visually:

Phase 3: Inflated Purchase Price

When demand starts becoming fueled by the expectation of price increases, rather than by local residents desire to move in and their ability to afford it, home prices start inflating artificially. Some buyers reach beyond their comfortable budget, aided by low-down-payment loan programs and loose income requirements.

And it works — for a little while. It creates a self-fulfilling prophecy, a feedback loop of higher prices fueling more demand with the expectation of further appreciation.

It doesn’t last.

Phase 4: The Bubble Bursts

Once homebuyers and speculators realize it costs more to live in the neighborhood or city than it’s actually worth, demand begins to dry up. Prices stagnate briefly, then when sellers can’t find a buyer, they lower their prices. It happens slowly at first, but once it becomes clear that there’s no demand at current pricing, demand falls even further.

Some homeowners end up underwater on their mortgages as prices fall. If they start defaulting on their loans, a wave of lower-cost foreclosures hit the market, driving prices even lower.

Investors don’t want to touch the area, and homeowners won’t either until prices drop enough for them to feel like they’re “scoring a deal.” Which eventually happens: prices go so low that the neighborhood becomes attractively priced again.

And the cycle starts anew.

(article continues below)

Real estate investments? Awesome.

Being a landlord? Less fun.

Learn how to earn 15%+ on passive real estate investments in our free video course.

The Case for a Housing Bubble in 2023

We did see nationwide home prices drop briefly from mid-2022 to early 2023. From a prior peak of $338,174 in August 2022, median home prices dipped to $331,792 by the end of March 2023. But let’s not dive for our apocalypse bunkers just yet. They subsequently turned upward again to close 2023 at $342,684. That’s an all-time high, for the record. Could real estate prices drop again? Absolutely. Will they drop 25-30% like they did in the Great Recession? Almost certainly not. The odds of a nationwide Great Recession-level housing bubble remain slim. That housing market crash resulted from a perfect storm of loose lending practices and poorly-regulated investment bankers selling derivatives that no one else understood. But when prices increase at a double digit pace for several years like they did from 2020-2022, alarm bells should ring. At the very least, it calls for deeper research into a potential housing crash in 2024.Ratio of Home Prices to Incomes

The median home price at the end of 1984 was $78,300. Adjusting for inflation, that comes to $225,457 in today’s dollars. By the end of December 2023, the median home price had jumped to $342,684 — a jump of 46.3%. Inflation-adjusted incomes, meanwhile, rose from $55,828 in 1984 to $74,580 in 2022 (the most recent data available from the Census Bureau). That’s an increase of 26.8%. While you probably didn’t know the exact numbers, you already knew that home prices have grown far faster than incomes over the last 40 years. And if that difference in growth seems small, take a look at this graph for a nasty dose of reality (the red line represents home prices):

It makes you wonder how much longer Americans can keep paying such a high multiple of their income for housing.

Is There a Real Estate Bubble in 2024?

The ratio of household incomes to home prices notwithstanding, I see a housing market correction in 2024, not a housing crash or real estate bubble.

Nor am I alone in that sentiment. The economists at Realtor.com forecast median home prices to dip by 1.7% in 2024, and rents to slip an average of 0.2% lower nationwide.

Zillow sees home prices largely ending the year flat from where they started it. In fact, analysts at Zillow already see the housing correction winding down.

Housing Inventory

Low housing inventory continues to buoy real estate values. While Realtor.com forecasts existing home sales to stay flat at 0.1%, they also expect inventory will plummet 14.0% over 2024.

The simple fact is that the U.S. continues to have a housing shortage. In the ten years from 2012-2021, the country added 12.3 million new households, but only 7 million new housing units — a shortfall of 5.3 million homes. A 2022 report by Up for Growth estimates the country’s housing shortage at 3.79 million units.

And don’t expect a glut of new homes to hit the market, either. Housing starts remain far below pre-pandemic levels.

Interest Rates & Recession Fears

That said, high and growing interest rates will act as a headwind limiting home price growth. Mortgage rates will continue climbing as the Federal Reserve continues its crusade against inflation, although most economists expect rates to start dipping by the end of 2024.

Of course, a proper recession would change the calculus. Far fewer people will feel comfortable shelling out huge sums for homes or rents, or indeed able to make their monthly payments. High unemployment rates would become high foreclosure rates, driving down real estate prices.

Don’t expect a Great Recession-style foreclosure boom though. Lending practices remain tighter than in 2006, despite loosening over the last five years.

Despite recession fears, U.S. gross domestic product (GDP) keeps improving. And while low by historical standards, the University of Michigan Consumer Sentiment Index has risen since an all-time low last July.

In short, most housing markets across the U.S. aren’t in freefall, despite what you read in the news.

To find undervalued markets, see our research and lists of the best cities for real estate investing in 2024, and the cheapest real estate in the US.

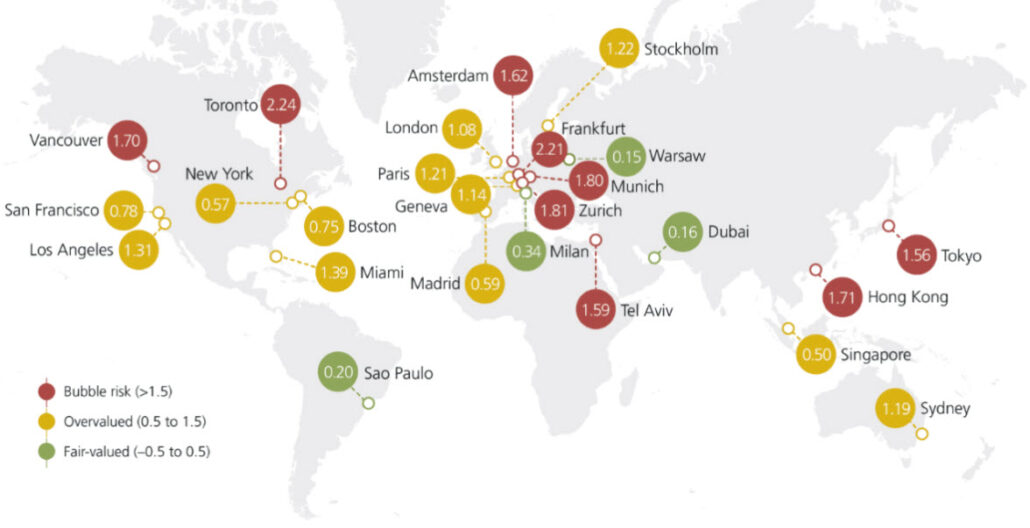

Annual UBS Report

Every year, UBS releases a report measuring housing bubble risk in cities across the world. The 2023 UBS report marks several U.S. cities as “overvalued,” but none at risk of a bubble. UBS bases their bubble risk index on five standardized city sub-indexes: price-to-income and price-to-rent (fundamental valuation), change in mortgage-to-GDP ratio and change in construction-to-GDP ratio (economic distortion), and relative price-city-to-country indicator.

Millennials Reaching Prime Homebuying Age

Millennials now make up the largest generation in the US. And with most now in their 30s (and early 40s, as I can attest), they’ve all reached their prime homebuying years.

Despite all the speculation back in the early 2010s, millennials really do want the same suburban lifestyle as their parents and grandparents before them. They want to grill burgers in the backyard, with their golden retriever and 2.1 kids. And many of them are first-time buyers, moving from urban apartments to larger homes in the ‘burbs.

All of which continues to drive demand among prospective buyers.

(article continues below)

What short-term fix-and-flip loan options are available nowadays?

What short-term fix-and-flip loan options are available nowadays?

How about long-term rental property loans?

We compare several buy-and-rehab lenders and several long-term landlord loans on LTV, interest rates, closing costs, income requirements and more.

How to Invest in a Housing Bubble

Worry a housing bubble is about to burst?

While I don’t see a real estate bubble in 2023, you might. Understand what investing through a bubble should look like, and how to protect yourself.

Buy Discounted Properties, Rather than Trying to Time the Market

First, don’t attempt to time the market. Market timing usually comes down to luck, and most of the time you’ll miss out on large market moves in pursuit of short-term gains.

If you wait for the next dip to buy, it could be years away. By that time, even the low point in the dip could mean higher prices than today’s values. Alternatively, if you rush to jump into a rapidly appreciating market, you risk buying in the midst of housing bubble mania.

Instead, dispassionately look for an investment that you can buy at a discount from market value. See our guide to finding deals on real estate even in a hot market for specific tactics, and look for motivated sellers. You can use an online tool like Propstream to find them instantly (full Propstream review here), or stick with classic strategies like driving for dollars or buying foreclosures.

For those of you who invest in stocks, think of it like value investing. Even in 2006 when home prices peaked, there were still plenty of undervalued markets and individual homes. From peak to trough of the housing crisis, the state of North Dakota averaged only a 2% decline in property value.

Avoid Speculation

Look for markets with steady but reasonable gains, rather than sharp spikes in home values. Sudden leaps in pricing often mean a divergence between incomes and home values.

Your real estate investments make up one part of a larger portfolio. Just like selecting stocks, you don’t want to speculate a large part of your portfolio.

Invest for Cash Flow

Most of all, to survive a housing bubble you’ll want to identify properties with strong rental cash flow. Rents tend to remain stable or even increase through any economic cycle. Even during the Great Recession and housing bubble of 2008, rents did not decline – they simply grew less quickly than they did previously. In a recession and real estate bubble, some homeowners end up becoming renters, which fuels demand for rental housing even as buyer demand dips.

The moral of the story: aim to buy properties that become real estate cash flow machines! Properties you can buy below-market value, but for the right reasons. It can be a real estate market that’s not seen by investors, small communities or a location that ignores typical recession factors.

Fortunately, you can calculate a property’s cash flow before buying. Use our free rental property calculator to run the numbers on any property, and never buy a bad deal again.

For more tips for investing in any phase of the housing cycle, see our tips for making money during housing market corrections.

Final Thoughts

Does the U.S. face a housing crash in 2024? I believe the odds are low, at least as a nationwide housing bubble in the U.S. The economy continues to expand, and the supply of homes doesn’t meet current demand. Subprime mortgages make up a much smaller percentage of the total outstanding loans on the market.

Still, do your due diligence when evaluating potential deals. Make sure you have a firm understanding of the local market. When you know the local market and the prospective property well, you can predict your cash flow and returns accurately.

And in doing so, protect yourself from losses in the next recession or housing bubble.♦

Do you think your home city is in a housing bubble about to burst? Why or why not? Share your thoughts below!

More Savvy Real Estate Investing Reads:

I want to know more about…

Connect with us on social!

Nice! So many of us worry about this, when in fact, like you say in this article. If you wait for the next dip to buy, it could be years away. like they say “Don’t wait to buy real estate, buy real estate and wait.” It’s better to look for great value, then worrying about what could happen. Everything has its risks, but we can’t let that fear hold us back.

So true Heather! And I love that saying, by the way 🙂

Thanks for sharing such things.

Glad you enjoyed the piece Frank!

The index of consumer sentiment dropped to 89.1 in March — its lowest level since October 2016 — from 101 in February.

March’s decline in sentiment was the fourth-largest in nearly 50 years, according to Richard Curtin, chief economist for the Surveys of Consumers.

Scary stuff. I do think we’ll see a softening in home prices in the wake of COVID-19, but I also think they’ll rebound with a vengeance later on. Far too little homebuilding activity going on right now, so supply is faltering, especially among starter homes.

We certainly live in interesting times.

What about the great baby boomer die off. Millions of properties will saturate the market at a rate greater than the greatest building boom. Not sure when it will happen but it is coming.,

It won’t happen all at once though. Many boomers are continuing to live in their homes, others gradually downsize. I personally think it will be spread out enough that it won’t create a massive oversupply.

Though as has already been admitted to, by several sources, supply increases will be heavier in some locales as opposed to others (same as booms also ebb and flow, alteratively). Plan ahead, and opportunity awaits. The housing bubble is just different this time, but it certainly is still there. Liken it to hunting by migratory patterns, haha.

Whatever happens, it’s better to be prepared in the next recession or housing bubble.

Absolutely Chelsea!

Reading this article is a relief against all the warnings about global inflation, market crash, and other scare tactics.

Thanks Theresa!

The only way to survive this present chaotic real estate market is to go for off-market! That is when community, landlord network, and other useful resources comes to play. We have technology to beat the market.

Yeah the best deals are usually off-market deals. What tech tools are you currently using to score off-market deals Alfonso?

I see a slow grind of crashing of residential real estate especially in areas where 2nd homes are like florida and the resort areas. In no way will the tripling and quadrupling of these prices remain so. The prices will revert back to its 2019 trend line at best.

Thanks for the input Realspert. I don’t think home prices in most real estate markets will drop back to 2019 levels, but I could certainly be wrong. Time will tell.